The Money Mindset

7 Expense Allocation

Anne Lee

Tracking expenses into categories in your budget will assist you in staying focused on financial goals and support having sufficient funds to meet payment due dates.

A popular budget allocation methodology is the 50/30/20 rule, as outlined in the book All Your Worth: The Ultimate Lifetime Money Plan by Elizabeth Warren. The framework for this rule is to apportion 50% of your after-tax income to Needs, 30% to Wants, and then a 20% allocation to Savings.

- 50% Needs: This would include expenses that are required to survive or must be paid to keep living the same lifestyle. Examples of needs in this category include rent/mortgage payments, car payments, groceries, utilities, basic phone/internet charges, and minimum debt payments.

- 30% Wants: Wants are considered expenses that are not essential or mandatory. These items are considered optional or in the ‘nice to have’ category. Eating at a new brunch place over cooking at home, and getting a taxi instead of taking public transit would fall into the Wants category. A few examples of Wants may include vacations, the latest technology gear, extravagant restaurant dinners, and concert tickets. Wants tend to make an individual’s lifestyle more enjoyable and comfortable.

- 20% Savings: The savings category is the one channel that is most important for building your financial future. Allocation of the budget to savings entails funds to fill an emergency fund, making contributions to a tax-advantaged account, investing in marketable securities, and making debt payments higher than the minimal monthly payment amount.

Example: 50/30/20 Allocation

George is a junior level tool and die maker apprentice in Ontario, and estimates his gross earnings this year will be $42,500. George’s income tax for the year is approximately $8,500. George strives to allocate the annual salary in the budget as follows:

| After-Tax Income ($42,500 less $8,500) | $34,000 |

| Needs (50%) | 17,000 |

| Wants (30%) | 10,200 |

| Savings (20%) | 6,800 |

The savings rate represents the amount of after-tax income dedicated to savings, expressed as a percentage. Following the 50/30/20 rule, the savings rate would be loosely calculated as 20%. However, it is recommended to only include items into the savings rate calculation that would build your net worth. Putting funds aside for the next planned vacation or towards a larger vehicle should be placed into the Wants category. Paying off credit card debt above the minimum payment amount that has already been accumulated should not provide the false impression that one is better-off at saving more. Therefore, most debt repayments are not included in the calculated savings rate.

Example: Savings Rate

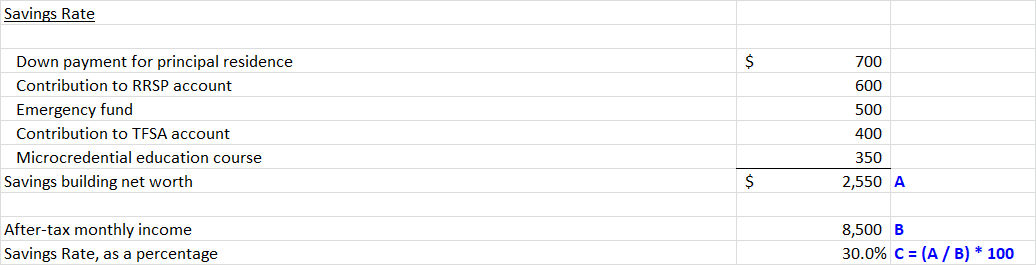

Matthew has after-tax monthly income of $8,500 working as a heavy equipment operator during a busy construction project with lots of overtime work. Matthew has allocated the following amounts to the monthly budget:

| Planned vacation to a sunny destination | $300 |

| Down payment for principal residence | $700 |

| Minimum payment amount to the credit card | $200 |

| Contribution to RRSP account | $600 |

| Emergency fund | $500 |

| Paying down further outstanding credit card balance | $250 |

| Contribution to TFSA account | $400 |

| Savings towards further trades training (microcredential course) | $350 |

Matthew’s savings rate for the month is calculated as follows:

Matthew would not include amounts towards a planned vacation or to pay off credit card balances as part of the savings rate determination. Investing into a principal residence may entail the house to increase in value over time and Matthew can make a higher wage with a further microcredential certification course. Both of these savings plans would increase Matthew’s net worth and so are included into the determination of savings rate.

Matthew would not include amounts towards a planned vacation or to pay off credit card balances as part of the savings rate determination. Investing into a principal residence may entail the house to increase in value over time and Matthew can make a higher wage with a further microcredential certification course. Both of these savings plans would increase Matthew’s net worth and so are included into the determination of savings rate.

Tax Tip: Tax-Advantaged Accounts

Funds allocated to savings can be put into a tax-advantaged account. Some very popular Canadian tax-advantaged accounts include the Registered Retirement Savings Plan (RRSP) and the Tax-Free Savings Account (TFSA). There are many benefits to utilizing a tax-advantaged account, which will be discussed further in Chapter 7 – Saving for the Future. It may be more beneficial to contribute as much savings as allowed to these tax-advantaged accounts over other savings categories.

In a Canadian economy with rising housing costs and skyrocketing inflation on basic necessities such as groceries, it is getting much more difficult to apportion only 50% of take-home pay to required needs. Trade apprentices or people who have accumulated some debt may find an allocation of 70/20/10 more feasible. Following a 70/20/10 apportionment of after-tax income would mean allowing 70% to cover necessities, 20% for comfort items, and dedicating 10% to savings. It is recommended for trade apprentices to seek funding opportunities available to assist in the periods of technical block training or when apprenticeship hours may not be as readily available. Chapter 5 – Funding Opportunities for Apprentices and Chapter 6 – The World of Debt will outline a number of avenues trade apprentices can take in seeking financial aid.

A savings rate template (Excel) has been provided that includes common savings items for trades workers.

Chapter 02_Savings Rate Template

Building an Emergency Fund

Let’s face it. Life happens and unexpected expenses arise that you may have to deal with. For trades workers, jobs may not be as available in certain unfavourable economic times. It is important to have an emergency fund set aside to pay for these unforeseen circumstances. Situations when this fund may be useful include:

- Vehicle break down

- Need to visit veterinarian to care for pets

- Employment loss or decrease in hours

- Accidents that require uninsured dental care

Having an available emergency fund lets you cover these sudden expenditures without having to get into increased amounts of debt or use credit cards which have a high-interest rate. It is recommended to have an emergency fund of at least 3-6 months of expected expenditures. Dealing with an emergency is stressful already. Ensuring you can cover any surprising financial situations will provide added peace of mind and an increased financial control mindset.

Example: Emergency Fund Amount

Kelly is building up an emergency fund. Kelly has reviewed her expenditures of the last few months and spends approximately $3,500 each month. Kelly should aim to have an emergency fund of at least $10,500 to $21,000 available.

- 3-months ($3,500 x 3 months) $10,500

- 6-months ($3,500 x 6 months) $21,000

It is highly recommended to initially build an emergency fund of $1,000 to $1,500 in the beginning stages of savings. The majority of emergencies will fall below this $1,000 threshold, and one will be able to have sufficient available funds if such a necessity arises.

Tax Tip: Interest Income

Emergency funds saved inside a high-interest savings account will earn interest income. This interest income is subject to income taxes in the year that it is earned. If the amount earned in the account is at least $50, then the financial institution will issue a tax slip to the individual to be reported on the Income Tax and Benefits Return (T1). Income taxes owed would be due by the following calendar year April 30th, with the tax return filing. When building an emergency fund, it is important to budget for these upcoming taxes due. Thus, your emergency fund may not have attained your goal balance from just what is showing in the account.

Example: Tax on Interest Income

Kelly has now saved the emergency fund to a $21,000 balance in a high-interest savings account for the entire year earning 5% interest annually. Assuming Kelly’s interest income would be subject to a 35% tax rate, Kelly would have the following emergency fund balance, interest earnings, and tax compliance obligations:

| Description | Amount | Balance Account | Notes |

| Earning interest income ($21,000 x 5%) | $1,050.00 | $22,050.00 ($21,000 + $1,050) | Calendar Year 2024 |

| Issued tax slip from financial institution | 1,050.00 | $22,050.00 ($21,000 + $1,050) | By end of February 2025 |

| Income tax return filed and taxes due ($1,050 x 35%) | $375.50 | $21,674.50 ($22,050 – $375.50) | By end of April 2025 |

Note: Not taking into consideration any further interest income earned in 2025.

the percentage of after-tax income that is put towards savings

the value of net assets that an individual has calculated by total assets less total liabilities

a retirement savings and investment plan that individuals can open an account for and contribute to. Deductible contributions can be used to reduce your income tax.

a registered savings account that individuals 18 and over with a valid Social Insurance Number (SIN) can open to set money aside tax-free throughout their lifetime

the Canadian tax return that individuals complete every year to calculate whether they owe tax on their income. A return must also be completed and submitted to Canada Revenue Agency to receive federal and provincial or territorial benefits and credits.