33 The Impact of Trust Building on Transaction Activity: A Study of Non-Fungible Token Projects [Award Winning Paper]

Andrew Park; Jan Kietzmann; and Leyland Pitt

*Best Paper Award for the Originality of Topic

Abstract

Non-fungible tokens (NFTs), which are digital assets such as art pieces and in-game collectibles secured by the blockchain and traded on decentralized marketplaces, have recently garnered tremendous public interest, highlighted by a digital art piece selling for $69.3 million USD in March 2021. NFTs and related decentralized platforms have significant implications for scholars, practitioners and policymakers whose industries may be affected by its continued emergence. Like traditional online marketplaces, trust plays an important role in whether a consumer decides to participate in the NFT ecosystem. However, existing management trust theory on online marketplaces is inadequately positioned to explain the role of trust in NFT ecosystems, due to the fact that there is no central authority to which a defrauded consumer can appeal, and the disparate transaction dynamics between buyers and sellers. Scraping online databases containing real-time data on global NFT projects and their transactions, we hypothesize, present and empirically test a novel model on the effects of trust building activity on transaction activity. We find that, for NFT projects, trust building activity is positively associated with transaction activity. However, this relationship is moderated by the average transaction size, i.e., the link between trust building activity and transaction activity is more pronounced for NFT projects that have large average transaction sizes. As far as we can ascertain, our study is the first that empirically tests the role of trust in the adoption of novel, decentralized online platforms. Our study has implications for practitioners who wish to successfully commercialize novel NFT or blockchain-based products, and for policymakers who wish to effectively support and regulate the burgeoning blockchain ecosystem.

Keywords: non-fungible token, trust, transaction-cost economics, blockchain, decentralized platform, online marketplace

Statement on Applied Research

This work is an applied research paper that advances current management theory on trust building in online marketplaces. We draw from Gefen & Pavlou’s (2012) theory that the relationship between trust and transaction activity is moderated by consumers’ perceived effectiveness of institutions. However, we argue that this theory does not adequately explain trust building activities in the context of decentralized marketplaces. We propose and empirically test a new theory using the rapidly rising NFT ecosystem as our context. This is heavily applied research as the NFT sector is a specific decentralized ledger (i.e., blockchain) application, and we test and apply existing and new management theory to derive our conclusions. Our applied study is empirical and quantitative in nature and aims to elucidate the role trust plays in transaction activity in novel, decentralized information systems.

Introduction

Non-fungible tokens (NFTs) are blockchain-backed digital assets that can represent ownership of images, videos, songs, privileges in video games and metaverses and more. It can be even be used to dematerialize and digitally represent physical assets in the real world, for example, to enable a decentralized land registry, which is currently being piloted in Honduras (Lemieux, 2016). While the existence of NFTs can be traced back to early blockchain projects such as CryptoPunks and Cryptokitties, interest in this blockchain application has generally been constrained to cryptocurrency enthusiasts, blockchain researchers and cryptographers. However, since early 2021, NFTs have started to receive much wider attention within broader technology communities and even the mainstream media. It has, in part, renewed general interest in blockchain technologies after a previous lull in the blockchain hype cycle due to declining cryptocurrency asset prices (which have since recovered dramatically) and disillusionment with the oversupply of questionable Initial Coin Offerings (ICOs).

Like predicate blockchain applications such as cryptocurrencies, distributed file storage and democratized personal health information, the adoption of NFTs is heavily reliant on consumer trust. This is consistent with the extensive literature on the importance of trust in the adoption and proliferation of novel information technologies (Komiak & Benbasat, 2006; Chopra & Wallace, 2003; Gefen, Straub & Boudreau, 2000; McKnight, Choudhury & Kaemar, 2002; McKnight, Cummings & Chervany, 1998; Garaus & Treiblmaier, 2021; Yang et al., 2021; Bapna, Qiu & Rice, 2016; Ananthakrishnan, Li & Smith, 2020; Gefen & Pavlou, 2012). The role trust plays in the continued growth of the NFT ecosystem is likely even more salient given the anonymity of the individual participants that secure a large blockchain network. Thus, it is important for firms and industries to understand the role of trust in emerging technology-based ecosystems such as NFTs in order to attract users and increase the adoption of their novel technologies.

NFTs began receiving growing media attention in early 2021 but sparked mass curiosity in March 2021, when an artist named Beeple sold a digital image at Christie’s for $69.3 million USD. This was the first instance of a digital asset being sold at such a price without an accompanying digital certificate of authenticity (Crow & Ostroff, 2021). Instead, ownership of Beeple’s digital art piece is documented on the Ethereum blockchain, where the record of the art piece is linked to a digital private key, which is owned by the buyer. NFTs need not be restricted to facilitating markets for digital art pieces or collectibles. They can be used to represent and transfer ownership of physical assets such as land parcels, to grant expanded privileges in online games and to enable more efficient transfers of web-based assets such as domain names. The popularity of NFTs has been accelerating rapidly; while the lifetime total traded volume of NFTs is $550 million USD, $200 million of that volume occurred in March 2021 alone (Dowling, 2021a). Other proxies for interest in NFTs exhibit similar patterns: Google Trend data shows little interest in NFTs until January 2021 and news media interest has exhibited similar trends (Dowling, 2021b).

Because of the novelty of NFTs, the literature on their implications to management is limited. Most of the existing research related to NFTs focuses on hypothetical, or proof-of-concept applications of the technology in various industries (Regner, Urbach & Schweizer, 2019; Chevet, 2018; Omar & Basir, 2020), on the technical aspects of NFTs (Hong, Noh & Park, 2019; Park, 2019; Bal & Ner, 2019) or on the relationship between NFTs and the value of cryptocurrencies such as Bitcoin, another closely related, more established blockchain application (Shirole, Darisi & Bhirud, 2020; ElMessiry & ElMessiry, 2019). Little research has been conducted on what factors facilitate the rapid adoption of a little known, highly inventive, distributed information technology. Namely, it is unclear how a technology ecosystem that is predicated on a large, decentralized network of untrusting parties such as NFTs creates and captures value.

If a firm wishes to operate and thrive in a novel, trust-less environment, it is likely that it must engender trust in its potential users and customers. Limited insights from prior literature on how to increase adoption of a novel information technology in trust-less settings leaves managers in the dark about how to develop strategies to accelerate the uptake of the technology. Thus, the relationship between a firm’s efforts in establishing trust in a novel, decentralized technology and the resultant value capture from these actions merits deeper investigation. Additionally, this research would be helpful to policymakers who wish to foster the growth of modern, decentralized business models such as NFTs and peer-to-peer asset sharing but also regulate them to ensure consumers are protected when participating in the ecosystem.

The objective of our research is to fill these knowledge gaps by providing novel, empirical insights into the relationship between NFT projects’ efforts to improve trust and the uptake of their products, and how the nature of those products affects this relationship. Formally, our research questions are: 1) Is there a relationship between efforts to improve trust and product adoption for NFT projects and firms? and 2) Do the characteristics of the NFT product moderate this relationship?

To address these research questions, we draw from the web-based database nonfungible.com, which is the preeminent and most comprehensive data source for NFT projects. This database aggregates and tracks transactions related to all public NFT projects and updates the data in real-time. The transaction records are sourced from the public ledger; for example, all transactions for the Cryptopunks project are recorded on the Ethereum blockchain, and nonfungible.com filters transactions on the Ethereum blockchain for only the ones related to Cryptopunks. All transactions for the 130 NFT projects listed on nonfungible.com are tracked and published in real-time.

We extract transaction volumes for each of these projects as a natural proxy for product adoption. We further operationalize our research agenda by collecting data on each project’s social media activity, specifically the number of Twitter followers as a proxy for the effort the project expends in signalling trust to its existing and future users. The use of social and traditional media platforms is a well-established technique in signalling project awareness and trust in the blockchain ecosystem (Wang & Vergne, 2017; Cheung, Roca & Su, 2015; Kristoufek, 2013; Barford, 2013). Since there is a wide variation in the price of a typical transaction among NFT projects (the previously noted example of an art piece selling for $69.3 million USD is contrasted by transactions within NFT games and virtual worlds, which can be as low as $0.35 USD), we calculate the average price of a transaction for each project to determine if there is a heterogenous treatment effect on the relationship between effort in establishing trust and product adoption.

Our study makes several contributions to management and information systems literature. First, we extend the management literature related to trust in technology product adoption by proposing a new theory explicating why efforts in increasing trust affect product adoption, and how this relationship is moderated by the size of transactions. Second, to support our theory, we examine a highly novel context that is based on a wide, decentralized network of untrusting parties. As far as we can ascertain, we provide the first quantitative, empirical study on NFTs; to date, we were only able to find conceptual studies related to the technical aspects or hypothetical applications of NFTs. This new context encourages further research from the scholarly community on the boundary conditions of existing management trust theories. Third, we inform business managers and policymakers on ways to leverage the increased digitization of numerous industries, specifically with respect to the anticipated growth of sectors based on dematerialized assets (Qi & Tao, 2018; Roquilly, 2011; Animesh, Pinsonneault & Yang, 2011; Chaturvedi, Dolk & Drnevish, 2011; Srivastava & Chandra, 2018). Effectively managing new technologies based on the growing decentralized platform industry can provide innumerable benefits to burgeoning firms in this sector and provide opportunities to grow existing information technology industries and create knowledge-based jobs.

Literature Review

In this section we review the literature from which we draw for our study. We begin by reviewing the management research landscape related to the role of trust in the adoption of novel information technologies. Following that, we review recent research on the role of trust in product adoption, specifically as it relates to blockchain and decentralized technologies. In each subsection, we identify the gaps in these bodies of literature, and how our study addresses them.

Research on Trust Related to Information Systems

There is an existing body of literature in the information systems field that examines the role of trust in internet and web technologies, ranging from empirical studies to the development of theoretical constructs surrounding the impact of trust on consumer adoption of online platforms. Information systems researchers have often rooted their context-specific theories in the general management trust literature and have noted that it is sometimes a nebulous term that is difficult to define or measure (McKnight, Choudhury & Kacmar, 2002; Ananthakrishnan, Li & Smith, 2020; Gefen & Pavlou, 2012). Much of the early empirical research related to trust in information systems centered on online transactions in the e-commerce and retail domain (Brynjolfsson & Smith, 2000; Gefen, 2000; Gefen, 2002) which is justified given the growing presence of marketplaces such as eBay and Amazon at the time.

Since then, some additional contexts have been studied, such as those related to virtual worlds (Charturvedi, Dolk & Drnevich, 2011; Roquilly, 2011), social media (Mallipeddi et al., 2021) and crowdfunding (Gao, Lin & Wu, 2021), however, many contemporary empirical information systems research on trust are still centered on long-established, traditional technology platforms such as online marketplaces and those that facilitate consumer reviews (Mejia, Gopal & Trusov, 2020; Saifee, 2020; Ke, Liu & Brass, 2020). We did not find any recent empirical papers that developed theories on trust based on highly novel and uncertain technologies such as decentralized networks and NFTs, though we did find a theoretical trust-based study on peer-to-peer lending (Wu et al., 2021). The lack of empirical studies on highly novel technologies limits the external validity of the existing information systems theories on trust. We aim to introduce a novel context to the body of literature on trust to better elucidate the boundary conditions of the role trust plays in new technology adoption.

We draw inspiration from Gefen & Pavlou’s (2012) theory that buyers’ perceived effectiveness of institutional structures (PEIS) moderates the relationship between trust and transaction activity. The authors argue that the relationship between trust and transaction activity is significantly moderated by the buyer’s perception, namely PEIS, of whether the institutional structures in the marketplace of interest are sufficiently protective of consumers and conducive to reliable transaction activity. The authors go so far as to say that if buyers’ PEIS is so low and they feel highly vulnerable to the potential downsides of the transaction, they will be unwilling to transact at all and the relationship between trust and transaction activity is invalidated. If the buyer has full confidence in the institutional structures of the specified marketplace, the relationship between trust and transaction activity is similarly invalidated since the buyer faces no risk in the transaction.

This model is somewhat context dependent, however, as Pavlou & Geffen (2004) note that in online marketplaces, buyers rarely transact with the same seller more than once, which is not the case in our research context. Furthermore, the authors’ empirical work was focused on eBay and Amazon’s online marketplaces. Buyers in these marketplaces have contingencies in the event their transactions go awry, namely, they can escalate their issues to the customer service representatives at each of these companies and request refunds. While the PEIS framework is largely appropriate in this traditional online marketplace context, it is not extensible to NFT ecosystems, where because of their decentralized nature, many NFT projects do not have centralized authorities to which buyers can appeal. Moreover, buyers often transaction with the same seller repeatedly, for example, in the case of microtransactions within NFT games and metaverses, potentially changing the trust dynamic between buyers and sellers. Thus, we propose a new theory on trust and transaction activity in the subsequent Hypothesis Development section.

Research on Trust Related to Blockchain

While the amount of research on trust in the traditional management literature is robust, and some theoretical and conceptual research related to highly novel information technologies such as decentralized platforms (e.g., blockchain and NFTs) exists, empirical research in this context is scarce. In this subsection we present the available literature on trust as it relates to blockchain technologies, of which NFTs are a subset. Ransbotham et al. (2016) write in general terms about the importance of embracing blockchain technologies while also dissuading or deterring nefarious actors from participating in blockchain-based ecosystems. Similarly, Brynjolfsson, Wang & Zhang (2021) write about the potential of blockchain to create new markets and note the need for scholars to study ways in which ecosystems can prevent unwanted side effects such as social inequality and balkanization, but do not further investigate trust issues in this context. There are numerous other papers that study the role of trust in blockchain from a philosophical and conceptual standpoint (Werbach, 2018; Anjum Sporny & Sill, 2017; Casey & Vigna, 2018; Hammi et al, 2018), which is unsurprising given the core strength of the technology is its ability to support an efficient and fluid transactional network among a large, decentralized group of untrusting parties (Nakamoto, 2008). However, we were not able to identify any notable papers that test the role of trust in a decentralized network that are empirical in nature.

Papers theorizing on the application of blockchain to various industries are numerous, and in the information systems field, perhaps the most commonly studied context related to trust and blockchains is the sharing economy. Hawlitschek, Notheisen & Teubner (2018) conduct a literature review on blockchain and trust, specifically on the sharing economy. Again, it is notable that none of the 62 articles identified in the literature review are empirical in nature. We address the gap in the blockchain, management and trust literature by conducting the first quantitative, empirical study in this field. We do this by specifically focusing on NFTs, a novel and rapidly emerging subset of blockchain technology.

Theoretical Framework and Hypotheses Development

In this section, we present two hypotheses that lead to the development of a novel theoretical framework linking trust generating efforts and product uptake and the moderating role transaction size plays in this relationship. We test these hypotheses empirically to support our framework.

Our novel framework draws upon the work described previously by Gefen & Pavlou (2012). We believe their argument that perceived institutional effectiveness moderates trust and transaction activity lacks external validity in the NFT ecosystem for several reasons. First, the very decentralized nature of the NFT ecosystem is incompatible with the conditions of the authors’ study, which was based on the eBay and Amazon marketplaces. These marketplaces are governed by a central authority and any buyer who feels they have been shortchanged in a transaction can begin an appeals process to the marketplace’s customer service departments. An arbiter, who is an employee of one of these central authorities, will ultimately determine the validity of the appeal and will enact punitive or corrective measures to the offending seller or provide a refund to the buyer. In the NFT ecosystem, there is no central authority. Records of digital ownership are recorded on a distributed ledger, which is itself secured by a large group of anonymous miners. There is no central authority to which a buyer can appeal and thus all transactions are effectively final, placing even more importance on an NFT project’s ability to signal trust before or early in its formation to attract users.

Second, the authors note that in their study, buyers seldom transact with the same seller more than once. This is not true within the NFT ecosystem. Particularly in the case of NFT-based games and metaverses, the same vendor may sell digital assets to the same buyer dozens or hundreds of times. In this manner, the amount of due diligence a buyer conducts prior to participating in the NFT ecosystem plays a much greater role in the level of user activity in a given NFT project than for a buyer making a single purchase on eBay.

Third, transaction size in unaccounted for in the authors’ model. Regardless of the PEIS of eBay or Amazon for a given buyer, the relationship between trust and transaction activity is likely going to look very different given the size of the transaction. For example, a user who is purchasing a big-ticket item such as a car will likely conduct much more due diligence on the seller than if the user was purchasing a cheap, consumer good. The effect of transaction size, and the potential level of harm in a deal gone awry on trust and transaction completion has been studied in detail in the transaction-cost economics literature (e.g., Chiles & McMackin, 1996) and we believe it plays an important role in trust and information systems product adoption. Because of the fundamentally different preconditions between Gefen & Pavlou’s (2012) study and ours, we believe a new model is required to better elucidate the relationship between trust and transaction activity for decentralized technology ecosystems.

Our first hypothesis suggests a relationship between an NFT project or firm’s trust building activities and transaction activity, or usage, of their product. It is common practice for blockchain projects to invest significantly in trust building prior to the launch of their platforms, mostly through marketing efforts (Sharma & Zhu, 2020). The use of social media as a trust building tool for firms has been extensively studied and supported in numerous industries (e.g., Hakansson & Witmer, 2015; Monforti & Marichal, 2014; Liss, 2011; Valenzuela, Park, & Kee, 2019). Because of the decentralized nature of blockchain products, consumers are well conditioned to conduct significant due diligence on the trustworthiness of a product prior to purchasing it or participating in its ecosystem. Trust building activities by blockchain projects are mostly marketing driven, taking the form of social media engagement, wide distribution of a project whitepaper, and bounty programs for pre-participants to trial products, identify bugs and co-promote the project. These efforts are mostly conducted to increase transaction activity on the prospective blockchain project platform, which ultimately raises the aggregate value of the project (Sockin & Xiong, 2018; Li & Mann, 2017; Bakos & Halaburda, 2018). Therefore, we hypothesize that NFT projects or firms that engage in more trust building activity have higher levels of transaction activity on their platforms.

Hypothesis 1: Trust building activity has a positive effect on NFT transaction activity, i.e., NFT projects that engage in more trust building activities exhibit higher value capture than projects that engage in less trust building activities.

Our second hypothesis addresses the potential moderating effect of transaction size (i.e., transaction price, or product price) has on the relationship between trust building activity and transaction activity in NFT projects. Previous literature has shown that consumers engage in more due diligence prior to a transaction if the price of the transaction is high (Venkatesan, Mehta & Bapna, 2007; Ma & Seidmann, 2015; Ba & Pavlou, 2002). Conversely, when transaction costs are low, i.e., the punitive effect of not conducting adequate due diligence is low (e.g., the consumer is comfortable with the prospect of writing the deal off), the level of due diligence prior to the transaction decreases. We believe this behavior also takes place in the NFT ecosystem, given the lack of a central authority and the fact that a shortchanged consumer has little to no ability to appeal if their perceived outcome of the transaction is unfair. Therefore, we hypothesize that transaction size has a moderating effect on the link between trust building activity and transaction activity: the greater the transaction size, the stronger the link.

Hypothesis 2: The effect of trust building activity on NFT transaction activity is heterogenous across NFT projects with large and small average transaction sizes, such that it is stronger for projects with large transaction sizes compared to projects with small transaction sizes.

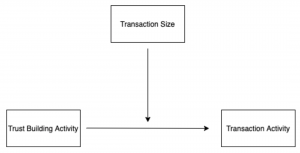

We capture these hypotheses in a novel, theoretical framework on trust in decentralized ecosystems, such as NFTs, and present it in Figure 1.

Figure 1 Trust Building Activity -> Transaction Activity Model

Methodology

In this section we describe the data sources, methods we used to collect the data, proxy variables chosen, characteristics of our dataset and the approach of our analysis.

Data

In order to create a comprehensive dataset containing existing NFT projects, we built a custom web scraper to track and pull data from nonfungible.com. Nonfungible.com is the largest and most prominent web-based database of global NFT projects and is the database most blockchain enthusiasts first consult to learn more about existing or forthcoming NFT projects. It operates by tracking the transaction ledgers of the major blockchain networks that house NFT projects through third party APIs and websites such as Etherscan, OpenSea, CoinGecko and Parity Ethereum (nonfungible.com, 2021) and publishing any new data in real-time. All data fields that are made available in this database were scraped, which include project name, project description, seven-day trading volume in US dollars, seven-day trading volume in number of transactions, all time trading volume in US dollars, all time trading volume in number of transactions, NFT type (e.g., art, game, utility, metaverse) and links to social media accounts. The most commonly available social media account was Twitter, and we followed each project’s Twitter link to extract the number of Twitter followers. We also followed the link to each project’s Github repository and collected the number of publicly published repositories; however, few projects had publicly published repositories so Github data did not factor into our final analysis. 130 total NFT projects were scraped from nonfungible.com. Out of these, 13 projects had missing or incomplete data and were discarded from our analysis, leading to a final sample size of 117 projects. A summary of the data fields collected on each NFT project is provided in Table 1. A table of ten sample projects, ordered by the highest seven-day trading volume in number of transactions is presented in Table 2.

Table 1 NFT Project Data Collected

| Field Name | Description | Data Type |

| Name | NFT project name | Text |

| Seven Day Trading Volume (US dollars) | Aggregate US dollar amount of all transactions in the past seven days |

Integer

|

| Seven Day Trading Volume (transactions) |

Total number of transactions in the past seven days |

Integer |

| All Time Trading Volume (US dollars) |

Aggregate US dollar amount of all transactions |

Integer |

| All Time Trading Volume (transactions) |

Total number of transactions | Integer |

| Type | Type of NFT project (e.g., art) |

Text |

| Twitter Followers | Number of followers on project’s Twitter account | Integer |

| Github Repositories | Number of publicly listed code repositories on project’s Github account |

Integer |

Table 2 Top 10 NFT Projects by Trailing Seven Day Transaction Volume

| Name | SevenDayVolume | Type | TwitterFollowers | GithubRepositorie |

| CryptoPunks | 13,133,226 | Collectible | 30,300 | 27 |

| Meebits | 5,419,573 | Collectible | 30,300 | 27 |

| SuperRare | 3,270,648 | Art | 1,256 | |

| Hashmasks | 342,806 | Art | 23,300 | |

| Decentraland | 787,061 | Metaverse | 133,300 | 156 |

| Sorare | 2,343,813 | Collectible | 29,500 | |

| CryptoKitties | 69,958 | Collectible | 38,700 | 87 |

| Art Blocks | 1,429,962 | Art | 13,200 | |

|

Gods Unchained |

14,127 | Game | 19,000 | |

| The Sandbox | 340,019 | Metaverse | 116,300 |

Proxy Variables

Our objective is to identify the impact of trust building activity for each NFT project on its transaction activity, so we choose the total number of transactions for each project as the dependent variable. We choose the aggregate number of transactions all time instead of the trailing seven-day number of transactions because it is more representative of total transaction activity of the NFT project and given the very young age of the ecosystem, there is little variability in project founding date among NFT projects. Since there is no concrete measure of trust building activity, we operationalize our research objective by using each project’s number of Twitter followers as a proxy to measure trust building activity. This proxy is supported by previous literature that indicates that most blockchain projects invest a significant amount of effort in social media marketing prior to, or early in a product launch (Cong & He, 2019; Sharma & Zhu, 2020; Sockin & Xiong, 2018; Li & Mann, 2018; Bakos & Halaburda, 2018), minimizing the effect of reverse causality (which is already mitigated by the fact that if our first hypothesis is supported, it will likely continue to be supported as the project matures) and that social media marketing in itself is an appropriate metric for measuring trust building efforts (Li & Mann, 2018; Hakansson & Witmer, 2015; Monforti & Marichal, 2014; Liss, 2011; Valenzuela, Park, & Kee, 2019).

Lastly, to examine the effect of transaction size as a moderator, we calculate the US dollar value of the average transaction size of an NFT project by dividing its all-time trading volume in US dollars by its all-time trading volume in number of transactions. To operationalize our research agenda, we wish to determine if there are interaction effects based on high dollar value transactions and low dollar value transaction, thus, we categorize the resultant average transaction sizes into large and small transactions in a dummy variable, using a cut-off of $50, which is a typical gas fee for an NFT asset transfer (Nftwars, 2021). A gas fee is paid on top of the price of the transaction by the buyer and is pooled by the blockchain network to incentivize miners to keep the network secure; this gas fee is not included in the average transaction size. We dichotomize the transaction size variable because of the likely psychological effect of the gas fee. The gas fee serves as a psychological benchmark for what a blockchain ecosystem participant may consider to be a small vs. large transaction size, as a transaction price lower than the gas fee is likely to be viewed as inexpensive. 59 of the 117 projects in our filtered sample were determined to be large transaction size projects and the remaining 58 projects were determined to be small transaction size projects.

Analysis

We conduct our analyses based on our filtered sample of 117 NFT projects, which is derived from the total sample of 130 projects, with 13 projects removed due to missing or incomplete data. We conduct an OLS regression to determine the relationship between trust building activity (operationalized as the natural log transformed number of Twitter followers) and transaction activity (operationalized as the natural log transformed total number of transactions). Our dependent variable, total number of transactions, and our independent variable, Twitter followers, are continuous variables. Our moderator variable, transaction size, is a dummy variable that indicates whether the project exhibits large or small transaction sizes. We conduct a moderator analysis to determine whether transaction size moderates the relationship between trust building activity and transaction activity by examining the statistical significance of the interaction term. We conduct post hoc probing by running separate regressions for NFT projects that have large transaction sizes and NFT projects that have small transactions sizes. Therefore, we model the dependent variable, transaction activity as follows:

transaction_activity = β0 + β1trust_building_activity + β2transaction_size + β3trust_building_activity *transaction_size

Results

In this section we present the results of our OLS regression to determine the relationship between trust building activity and transaction activity. We also present the results of our moderator analysis to determine the effect of transaction size on this relationship. We conclude by conducting post hoc analyses on our OLS regression, by conducting separate regression analyses for large and small transaction size NFT projects.

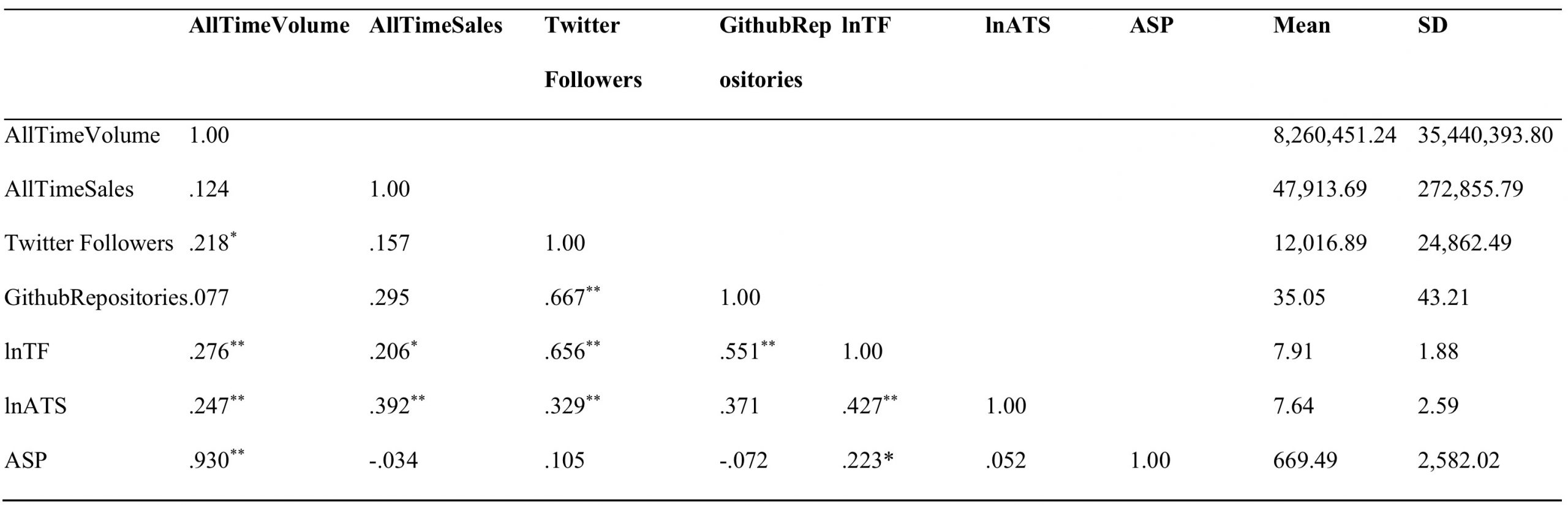

Table 3 shows descriptive statistics on the variables in our database and includes results of Pearson correlations. We observe significant and positive correlations between several of the variables that are tested in our OLS regression. For example, we see notable correlations between lnTF (natural log transformed number of Twitter followers) and lnATS (natural log transformed number of transactions) (r(117) = .427, p < 0.01) and lnTF and ASP (average selling price, or average transaction size) (r(117) = .223, p < 0.05).

Table 3 Descriptive Statistics

N = 117

** p < 0.01; * p < 0.05

Table 4 shows the results of our OLS regression with lnTF as our regressor and lnATS as our dependent variable. Referring to our model, we find the coefficient of trust_building_activity is positive (.751) and significant (p < 0.01), providing support for Hypothesis 1. In other words, the results suggest that an NFT project or firm efforts in building trust are positively associated with the usage of its platform. In order to draw inferences with respect to Hypothesis 2, we run a second regression model, with lnTF and DummyASP as an interaction term, i.e., we test whether or not the NFT project has large transaction sizes has a moderating effect on the relationship between trust_building_activity and transaction_activity. The results are presented in Table 5.

Again, referring to our mode, we find that the interaction between trust_building_activity and transaction_size has a positive coefficient (.520) and is significant (p < 0.05) for the effect of trust_building_activity on transaction_activity, hence whether or not the NFT project has large transaction sizes indeed has a moderating effect, and the direction of the moderation is positive. In other words, NFT projects with large transaction sizes enjoy a greater benefit of trust building activity on transaction activity than NFT projects with low transaction sizes. Hypothesis 2 is supported.

Table 4 OLS regression

| lnATS | |

| lnTF

|

.751**

(.116) |

N=117. Standard errors in parentheses.

** p < 0.01; * p < 0.05

Table 5 OLS regression with interaction term

| lnATS | |

|

lnTF

DummyASP

lnTF_x_Dumm yASP

|

.487**

(.162) -5.878** (1.847) .520* (.228)

|

N=117. Standard errors in parentheses.

** p < 0.01; * p < 0.05

We conduct post hoc probing to further investigate the moderating effect of large transaction sizes. We conduct separate regressions for NFT projects with large transaction sizes and NFT projects with small transactions sizes. The results are shown in Tables 6a and 6b, respectively. We note that NFT projects with large transaction sizes have a larger coefficient for lnTF (1.008) than NFT projects with small transaction sizes (.487), further supporting our observations related to Hypothesis 2. Namely, large transaction size NFT projects enjoy the benefits of trust building activities disproportionately compared to low transaction size NFT projects.

Table 6a OLS regression – large transaction size

| lnATS | |

| lnTF

|

1.008**

(.150) |

N=59. Standard errors in parentheses.

** p < 0.01; * p < 0.05

Table 6b OLS regression – small transaction size

| lnATS | |

| lnTF

|

.487**

(.172) |

N=58. Standard errors in parentheses.

** p < 0.01; * p < 0.05

Discussion

NFTs have been drawing considerable media attention in early 2021, and blockchain enthusiasts and speculators have noted the potential for NFTs to revolutionize the way we create digital assets and dematerialize existing physical assets. Because NFTs are an application of blockchain technologies, it enjoys significant advantages over traditional marketplaces and platforms for the exchange of goods, as it is secured by an immutable shared ledger, is not subject to the whims of any central authority, and it allows for instant verification of asset ownership through the use of cryptographically secure private keys. However, decentralization comes at a cost; because there is no central authority to which a defrauded buyer can appeal, as there is in the case of traditional online marketplaces such as eBay and Amazon, the consumer must conduct significantly more due diligence on the seller and the platform itself, before they feel comfortable engaging in a transaction and participating in the ecosystem.

In order for an emerging NFT project, or even an incumbent firm in a traditionally non- decentralized industry who wishes to participate in the blockchain ecosystem, to increase product adoption, it is evident that it must build trust in its prospective consumer base. Because of the newness of the NFT ecosystem, and even the blockchain ecosystem, there is very little empirical or quantitative scholarly work on trust models in decentralized platforms. The traditional trust literature in the management field offers a start to understanding the dynamics of trust in online marketplaces. We draw on Gefen & Pavlou’s (2012) model to inform our initial framework building efforts that are specific to our context. They suggest that buyers’ perceptions on the effectiveness of the institutions on which they’re relying (e.g., the policies and practices of eBay and Amazon) moderate the relationship between trust and transaction activity. However, we note that this theory is not extensible to NFTs, and decentralized marketplaces, for multiple reasons, including a) the fact that there is no institution, or central authority, to which a buyer can appeal and b) there are many repeated transactions between the same seller and buyer in decentralized marketplaces, especially for games (Gefen & Pavlou assume buyers rarely transact with the same seller). Therefore, one of our key contributions is the development of a new theory explicating the relationship between trust building activity and transaction activity, moderated by transaction size.

We further contribute to the trust literature by conducting one of the few quantitative, empirical studies on trust in blockchain applications, and likely the first on NFTs. We collect our data by scraping the most prominent web-based database tracking NFT projects and their associated transaction data. We augment the data with social media metrics such as the number of Twitter followers and the number of Github repositories to better understand the link between trust building activity and product adoption and usage. We also test the moderating effect of the average transaction size on each NFT project platform to determine if there is a heterogenous effect of trust building activity on transaction activity. We find that trust building activity is positively associated with transaction activity, but that this relationship is more pronounced for NFT projects that have large transaction sizes. Our work offers more clarity into the boundary conditions of management trust theory as it relates to online marketplaces; trust building activities in decentralized marketplaces have idiosyncratic effects on transaction activity based on transaction sizes and thus existing trust theory may not be universally applied to such ecosystems.

As our final contribution, we inform business managers and policymakers on how to effectively structure their decisions around the anticipated rise of decentralized technologies and the increased digitization of a swath of industries (Qi & Tao, 2018; Roquilly, 2011; Animesh, Pinsonneault & Yang, 2011; Chaturvedi, Dolk & Drnevish, 2011; Srivastava & Chandra, 2018). While NFTs are currently mostly associated with digital art pieces and collectibles, there are numerous pilot projects underway that are dematerializing physical assets, potential upending the way they are currently tracked. Some of these include replacing central land registries with blockchain-based records systems (Lemieux, 2016) and replacing and federating existing supply chain records with NFT-based certification systems (Ge et al., 2017). Managers who wish to participate in these burgeoning industries should recognize the importance of early trust building and realize that implementing even low-cost methods of engendering trust, such as having a consistent and active social media presence, may lead to competitive advantages in product adoption. Policymakers may create procedural infrastructures to ensure regulatory compliance by NFT projects and firms, which has the potential by-product of increasing consumer confidence and trust. Effective policy could encourage the creation of an efficiently regulated and rapidly growing new technology ecosystem, leading to public benefits and knowledge-based jobs. Early, facilitative government involvement in other technology-based industries such as biotechnology has been shown to be important in creating a vibrant ecosystem that disproportionately attracts highly skilled, knowledge-based workers and ecosystem participants such as venture capitalists and technology incubators (Etzkowitz & Zhou, 2019; Leih & Teece, 2016; Stern 2020).

Conclusion

Through examination of the emergence of a novel NFT ecosystem and the trust building and product adoption patterns and strategies of the firms within it, we find evidence of the importance of trust building activity conducted by NFT projects on product adoption and usage. We advance the conversation related to trust in the management literature by offering a new model on the relationship between trust building activity and transaction activity, and the moderating effect of transaction size. This model addresses some of the limitations on existing trust theory on traditional online marketplaces and is designed for novel and emerging contexts involving decentralized platforms. We observe that while trust building activity is positively associated with transaction activity, this link is more pronounced for NFT projects that have large transaction sizes.

In addition to our scholarly contributions and the fact that our study is one of the few quantitative, empirical studies on the role trust plays in blockchain, NFT and other decentralized platforms, our findings have important implications for practitioners and policymakers. Emerging decentralized platforms have significant economic potential and could spur the creation of completely new industries. In the case of NFTs, while their use is currently restricted to trading digital art, assets within games and other collectibles, it is already being piloted in large industries where the dematerialization of assets provides significant value, such as centralized land and property registries. The growth of these industries has significant potential for improved social and economic outcomes through more knowledge-based jobs and heightened interest from global researchers and technology industry participants. If our argument that trust building activity is positively associated with transaction activity, moderated by transaction size, is indeed important to the growth of the decentralized platform industry, then creating the conditions under which consumers can feel adequately protected when participating in new blockchain and NFT ecosystem should be a serious consideration for managers and policymakers alike.

References

Ananthakrishnan, U. M., Li, B., & Smith, M. D. (2020). A Tangled Web: Should Online Review Portals Display Fraudulent Reviews?. Information Systems Research, 31(3), 950-971.

Animesh, A., Pinsonneault, A., Yang, S. B., & Oh, W. (2011). An odyssey into virtual worlds: exploring the impacts of technological and spatial environments on intention to purchase virtual products. MIS Quarterly, 789-810.

Anjum, A., Sporny, M., & Sill, A. (2017). Blockchain standards for compliance and trust. IEEE Cloud Computing, 4(4), 84-90.

Ba, S., & Pavlou, P. A. (2002). Evidence of the effect of trust building technology in electronic markets: Price premiums and buyer behavior. MIS Quarterly, 243-268.

Bakos, Y., & Halaburda, H. (2018). The role of cryptographic tokens and icos in fostering platform adoption. Available at SSRN 3207777.

Bal, M., & Ner, C. (2019). NFTracer: a Non-Fungible token tracking proof-of-concept using Hyperledger Fabric. arXiv preprint arXiv:1905.04795.

Bapna, R., Qiu, L., & Rice, S. C. (2016). Repeated interactions vs. social ties: Quantifying the economic value of trust, forgiveness, and reputation using a field experiment. Forthcoming, MIS Quarterly, NET Institute Working Paper, (14-07).

Barford V, (2013, December 13). Bitcoin: Price v hype. BBC News Magazine. Retrieved from http://www.bbc.com/news/magazine-25332746.

Brynjolfsson, E., Wang, C., & Zhang, X. (2021). The economics of IT and digitization: Eight questions for research. MIS Quarterly, 45(1), 473-477.

Casey, M. J., & Vigna, P. (2018). In blockchain we trust. MIT Technology Review, 121(3), 10- 16.

Chaturvedi, A. R., Dolk, D. R., & Drnevich, P. L. (2011). Design principles for virtual worlds. MIS Quarterly, 673-684.

Cheung, A., Roca, E., & Su, J. J. (2015). Crypto-currency bubbles: an application of the Phillips–Shi–Yu (2013) methodology on Mt. Gox bitcoin prices. Applied Economics, 47(23), 2348-2358.

Chevet, S. (2018). Blockchain technology and non-fungible tokens: Reshaping value chains in creative industries. Available at SSRN 3212662.

Chiles, T. H., & McMackin, J. F. (1996). Integrating variable risk preferences, trust, and transaction cost economics. Academy of Management Review, 21(1), 73-99.

Chopra, K., & Wallace, W. A. (2003, January). Trust in electronic environments. In 36th Annual Hawaii International Conference on System Sciences, 2003. Proceedings of the (pp. 10-pp). IEEE.

Cong, L. W., & He, Z. (2019). Blockchain disruption and smart contracts.

Crow, K., & Ostroff, C. (2021). Beeple NFT fetches record-breaking $69 million in Christie’s sale. Wall Street Journal.

Dowling, M. (2021a). Is non-fungible token pricing driven by cryptocurrencies?. Finance Research Letters, 102097.

Dowling, M. (2021b). Fertile LAND: Pricing non-fungible tokens. Finance Research Letters, 102096.

ElMessiry, M., ElMessiry, A., & ElMessiry, M. (2019, June). Dual Token Blockchain Economy Framework. In International Conference on Blockchain (pp. 157-170). Springer, Cham.

Etzkowitz, H., & Zhou, A. (2019). Triple Helix : a universal innovation model ?. In Handbook on Science and Public Policy. Edward Elgar Publishing.

Gao, Q., Lin, M., & Wu, D. J. (2020). Education Crowdfunding and Student Performance: An Empirical Study. Information Systems Research.

Garaus, M., & Treiblmaier, H. (2021). The influence of blockchain-based food traceability on retailer choice: The mediating role of trust. Food Control, 108082.

Ge, L., Brewster, C., Spek, J., Smeenk, A., Top, J., van Diepen, F., … & de Wildt, M. D. R. (2017). Blockchain for agriculture and food: Findings from the pilot study (No. 2017-112). Wageningen Economic Research.

Gefen, D., Straub, D., & Boudreau, M. C. (2000). Structural equation modeling and regression: Guidelines for research practice. Communications of the association for information systems, 4(1), 7.

Gefen, D. (2000). E-commerce: The role of familiarity and trust. Omega, 28(6):725–737. Gefen, D. (2002). Reflections on the dimensions of trust and trustworthiness among online consumers. ACM SIGMIS Database, 33(3): 38–53.

Gefen, D., & Pavlou, P. A. (2012). The boundaries of trust and risk: The quadratic moderating role of institutional structures. Information Systems Research, 23(3-part-2), 940-959.

Håkansson, P., & Witmer, H. (2015). Social media and trust: A systematic literature review. Journal of Business and Economics, 6(3), 517-524.

Hammi, M. T., Hammi, B., Bellot, P., & Serhrouchni, A. (2018). Bubbles of Trust: A decentralized blockchain-based authentication system for IoT. Computers & Security, 78, 126- 142.

Hawlitschek, F., Notheisen, B., & Teubner, T. (2018). The limits of trust-free systems: A literature review on blockchain technology and trust in the sharing economy. Electronic commerce research and applications, 29, 50-63.

Hong, S., Noh, Y., & Park, C. (2019, December). Design of Extensible Non-Fungible Token Model in Hyperledger Fabric. In Proceedings of the 3rd Workshop on Scalable and Resilient Infrastructures for Distributed Ledgers (pp. 1-2).

Ke, Z., Liu, D., & Brass, D. J. (2020). Do Online Friends Bring Out the Best in Us? The Effect of Friend Contributions on Online Review Provision. Information Systems Research, 31(4), 1322-1336.

Kristoufek, L. (2013). BitCoin meets Google Trends and Wikipedia: Quantifying the relationship between phenomena of the Internet era. Scientific Reports, 3(1), 1-7.

Komiak, S. Y., & Benbasat, I. (2006). The effects of personalization and familiarity on trust and adoption of recommendation agents. MIS Quarterly, 941-960.

Leih, S., & Teece, D. (2016). Campus leadership and the entrepreneurial university: A dynamic capabilities perspective. Academy of Management Perspectives, 30(2), 182-210.

Lemieux, V. L. (2016). Trusting records: is Blockchain technology the answer?. Records Management Journal.

Li, J., & Mann, W. (2018). Initial coin offerings and platform building.

Liss, J. (2011). Negotiating the Marcellus: the role of information in building trust in extractive deals. Negotiation Journal, 27(4), 419-446.

Ma, D., & Seidmann, A. (2015). Analyzing software as a service with per-transaction charges. Information Systems Research, 26(2), 360-378.

Mallipeddi, R. R., Janakiraman, R., Kumar, S., & Gupta, S. (2021). The Effects of Social Media Content Created by Human Brands on Engagement: Evidence from Indian General Election 2014. Information Systems Research.

McKnight, D. H., Choudhury, V., & Kacmar, C. (2002). Developing and validating trust measures for e-commerce: An integrative typology. Information Systems Research, 13(3), 334- 359.

McKnight, D. H., Cummings, L. L., & Chervany, N. L. (1998). Initial trust formation in new organizational relationships. Academy of Management review, 23(3), 473-490.

Mejia, J., Gopal, A., & Trusov, M. (2020). Deal or No Deal? Online Deals, Retailer Heterogeneity, and Brand Evaluations in a Competitive Environment. Information Systems Research, 31(4), 1087-1106.

Monforti, J. L., & Marichal, J. (2014). The role of digital skills in the formation of generalized trust among Latinos and African Americans in the United States. Social Science Computer Review, 32(1), 3-17.

Nakamoto, S. (2008). Bitcoin: A peer-to-peer electronic cash system. Retrieved from https://bitcoin.org/bitcoin.pdf

Nftwars. (2021). NFTWars, transforming NFT gaming with Layer-2 blockchain technology. Retrieved from https://www.globenewswire.com/news-release/2021/03/19/2196067/0/en/NFTWars-transforming-NFT-gaming-with-Layer-2-blockchain-technology.html

Nonfungible.com (2021). What is NonFungible.com? Retrieved from https://nonfungible.com/about-us

Omar, A. S., & Basir, O. (2020). Capability-based non-fungible tokens approach for a decentralized AAA framework in IoT. In Blockchain Cybersecurity, Trust and Privacy (pp. 7- 31). Springer, Cham.

Park, C. (2019, December). Design of Extensible Non-Fungible Token Model in Hyperledger Fabric. In SERIAL 2019. ACM/IFIP.

Pavlou, P. A., & Gefen, D. (2004). Building effective online marketplaces with institution-based trust. Information systems research, 15(1), 37-59.

Qi, Q., & Tao, F. (2018). Digital twin and big data towards smart manufacturing and industry 4.0: 360 degree comparison. Ieee Access, 6, 3585-3593.

Ransbotham, S., Fichman, R. G., Gopal, R., & Gupta, A. (2016). Special section introduction— ubiquitous IT and digital vulnerabilities. Information Systems Research, 27(4), 834-847.

Regner, F., Urbach, N., & Schweizer, A. (2019). NFTs in Practice–Non-Fungible Tokens as Core Component of a Blockchain-based Event Ticketing Application.

Roquilly, C. (2011). Control over virtual worlds by game companies: Issues and recommendations. MIS Quarterly, 653-671.

Saifee, D. H., Zheng, Z., Bardhan, I. R., & Lahiri, A. (2020). Are Online Reviews of Physicians Reliable Indicators of Clinical Outcomes? A Focus on Chronic Disease

Management. Information Systems Research, 31(4), 1282-1300.

Sharma, Z., & Zhu, Y. (2020). Platform building in initial coin offering market: Empirical evidence. Pacific-Basin Finance Journal, 61, 101318.

Shirole, M., Darisi, M., & Bhirud, S. (2020). Cryptocurrency Token: An Overview. IC-BCT 2019, 133-140.

Sockin, M., & Xiong, W. (2020). A model of cryptocurrencies (No. w26816). National Bureau of Economic Research.

Srivastava, S. C., & Chandra, S. (2018). Social presence in virtual world collaboration: An uncertainty reduction perspective using a mixed methods approach. MIS Quarterly, 42(3), 779- 804.

Stern, S. (August, 2020). Accelerating Entrepreneurial Ecosystems: Lessons from the MIT Regional Entrepreneurship Acceleration Program. R&D Management Symposium, Virtual.

Valenzuela, S., Park, N., & Kee, K. F. (2009). Is there social capital in a social network site?: Facebook use and college students’ life satisfaction, trust, and participation. Journal of Computer-Mediated Communication, 14(4), 875-901.

Venkatesan, R., Mehta, K., & Bapna, R. (2007). Do market characteristics impact the relationship between retailer characteristics and online prices?. Journal of Retailing, 83(3), 309- 324.

Wang, S., & Vergne, J. P. (2017). Buzz factor or innovation potential: What explains cryptocurrencies’ returns?. PloS one, 12(1), e0169556.

Werbach, K. (2018). The blockchain and the new architecture of trust. MIT Press.

Wu, Z., Hu, L., Lin, Z., & Tan, Y. (2021). Competition and Distortion: A Theory of Information Bias on the Peer-to-Peer Lending Market. Information Systems Research.

Yang, M., Jiang, J., Kiang, M., & Yuan, F. (2021). Re-examining the impact of multidimensional trust on patients’ online medical consultation service continuance decision. Information Systems Frontiers, 1-25.