Part C – Understanding the Business of Managing

Chapter 16 – Money and Banking

Learning Objectives

- identify the functions of money and the different forms it takes in Canada;

- describe how government measures the money supply;

- distinguish among different types of financial institutions in the Canadian financial system;

- discuss the services that financial institutions provide in Canada;

- classify money supply into M-1 and M-2;

- identify the functions of the Bank of Canada and explain how it uses monetary policy to control the money supply and influence interest rates;

- discuss some of the institutions and activities in international banking and finance; and

- Explain key terms in the chapter.

Show What You Know

Show What You Know

Functions of Money

Finance is about money. So our first question is, what is money?

If you happen to have one on you, take a look at a $5 bill. Though this piece of paper — indeed, money itself — has no intrinsic value, it is certainly in demand. Why? Because money serves three basic functions:

- a medium of exchange;

- a measure of value; and

- a store of value.

To get a better idea of the role of money in a modern economy, let us imagine a system in which there is no money. In this system, goods and services are bartered — traded directly for one another. Now, if you are living and trading under such a system, for each barter exchange that you make, you will have to have something that another trader wants. For example, say you are a farmer who needs help clearing his fields. Because you have plenty of food, you might enter into a barter transaction with a laborer who has time to clear fields but not enough food: he’ll clear your fields in return for three square meals a day. This system will work as long as two people have exchangeable assets, but needless to say, it can be inefficient. If we identify the functions of money, we will see how it improves the exchange for all the parties in our hypothetical set of transactions.

Money is anything that is acceptable as payment for goods and services. It affects our lives in many ways. We earn it, spend it, save it, invest it — and often wish we had more of it. Businesses and government use money in similar ways. Both require money to finance their operations. By controlling the amount of money in circulation, the federal government can promote economic growth and stability. For this reason, money has been called the lubricant of the machinery that drives our economic system. Our banking system was developed to ease the handling of money.

Medium of Exchange

Money serves as a medium of exchange because people will accept it in exchange for goods and services. Because people can use money to buy the goods and services that they want, everyone’s willing to trade something for money. The laborer will take money for clearing your fields because he can use it to buy food. You’ll take money as payment for his food because you can use it not only to pay him but also to buy something else you need (perhaps seeds for planting crops).

For money to be used in this way, it must possess a few crucial properties:

- It must be divisible — easily divided into usable quantities or fractions. A $5 bill, for example, is equal to five $1 bills. If something costs $3, you don’t have to rip up a $5 bill; you can pay with three $1 bills.

- It must be portable — easy to carry; it can’t be too heavy or bulky.

- It must be durable. It must be strong enough to resist tearing and the print can’t wash off if it winds up in the washing machine.

- It must be difficult to counterfeit; it won’t have much value if people can make their own.

Measure of Value

Money simplifies exchanges because it serves as a measure of value. We state the price of a good or service in monetary units so that potential exchange partners know exactly how much value we want in return for it. This practice is a lot better than bartering because it’s much more precise than an ad hoc agreement that a day’s work in the field has the same value as three meals.

Store of Value

Money serves as a store of value. Because people are confident that money keeps its value over time, they’re willing to save it for future exchanges. Under a bartering arrangement, the laborer earned three meals a day in exchange for his work. But what if, on a given day, he skipped a meal? Could he “save” that meal for another day? Maybe, but if he were paid in money, he could decide whether to spend it on food each day or save some of it for the future. If he wanted to collect on his unpaid meal two or three days later, the farmer might not be able to pay it; unlike money, food could go bad.

The Money Supply

Now that we know what money does, let us tackle another question: how much money is there? How would you go about “counting” all the money held by individuals, businesses, and government agencies in this country? You could start by counting the money that’s held to pay for things on a daily basis. This category includes cash (paper bills and coins) and funds held in demand deposits — chequing accounts, which pay given sums to “payees” when they demand them.

Then, you might count the money that is being “saved” for future use. This category includes interest-bearing accounts, time deposits (such as certificates of deposit, which pay interest after a designated period of time), and money market mutual funds, which pay interest to investors who pool funds to make short-term loans to businesses and the government.

M-1, M-2 and M3

Counting all this money would be a daunting task (in fact, it would be impossible). Fortunately, there’s an easier way — namely, by examining two measures that the government compiles for the purpose of tracking the money supply: M-1 and M-2.

- M-1 is the narrowest measure, and it includes the most liquid forms of money — the forms, such as cash and chequing account funds, that are spent immediately.

- M-2 includes everything in M-1 plus near-cash items invested for the short term — savings accounts, time deposits and money market mutual funds.

- Canada Money Supply M3 includes M2 plus long-term time deposits in banks.

How much money is out there? Statistics Canada reports that as of April 2018, M-1, totalled $877 billion in Canada and M-2 totalled $1596 in Canada.[1] Also, Money Supply M2 in Canada increased to 2289771 CAD Million in October from 2286467 CAD Million in September of 2021.[2]

What, Exactly, Is “Plastic Money”?

Are credit cards a form of money? If not, why do we call them plastic money? Actually, when you buy something with a credit card, you are not spending money. The principle of the credit card is buy-now-pay-later. In other words, when you use plastic, you are taking out a loan that you intend to pay off when you get your bill. And the loan itself is not money. Why not? Basically, because the credit card company cannot use the asset to buy anything. The loan is merely a promise of repayment. The asset does not become money until the bill is paid (with interest). That is why credit cards are not included in the calculation of M-1 and M-2.

Financial Institutions

For financial transactions to happen, money must change hands. How do such exchanges occur? At any given point in time, some individuals, businesses, and government agencies have more money than they need for current activities; some have less than they need. Thus, we need a mechanism to match savers (those with surplus money that they are willing to lend out) with borrowers (those with deficits who want to borrow money). We could just let borrowers search out savers and negotiate loans, but the system would be both inefficient and risky. Even if you had a few extra dollars, would you lend money to a total stranger? If you needed money, would you want to walk around town looking for someone with a little to spare?

Now you know why we have financial institutions: they act as intermediaries between savers and borrowers and they direct the flow of funds between them. With funds deposited by savers in chequing, savings, and money market accounts, they make loans to individual and commercial borrowers. We will discuss the most common types of depository institutions (banks that accept deposits) and several non-depository institutions (which provide financial services but do not accept deposits), including finance companies, insurance companies, brokerage firms, and pension funds. The financial services industry in Canada continues to evolve, so some of the differences between institutions are disappearing. Also deregulation in the financial industry, advancement in technology and the changes in consumer demands, have enabled Canadian banks to diversify to provide more financial products and services to their customers and clients.

Chartered (Commercial) Banks

Chartered banks are the most common financial institutions in Canada, with total financial assets of about $2.39 trillion in February 2018.[3] They generate profit not only by charging borrowers higher interest rates than they pay to savers but also by providing such services as cheque processing, trust- and retirement-account management, and electronic banking. The country’s chartered banks range in size from very large (Royal Bank of Canada, Toronto Dominion Bank) to very small (such as Versa Bank). Because of mergers and financial problems, the number of banks has declined significantly in recent years, but by the same token, surviving banks have grown quite large. Banking is a competitive business, so chartered banks do not just provide short- and long-term loans or create money, but many other products and services, such as the following.

Electronic Funds Transfer: Electronic funds transfer (EFT) is the electronic transfer of money from one bank account to another, either within a single financial institution or across multiple institutions, via computer-based systems and telephones, without the direct intervention of bank staff. Transfers can take place between individuals or businesses, locally, nationally or internationally, and use various currencies. Formats include PayPal, Alipay and other electronic payments. EFT systems enable customers to use their debit cards and mobile devices to enjoy speed and convenience at checkouts instead of writing cheques. EFTs enable automatic payroll deposits, ATM transactions, bill payments, automatic funds transfer, etc. EFT has changed the way businesses and people interact online, and fosteredd e-commerce. Other examples include:

- automated banking machines (ABM) and automated teller machines (ATM);

- direct deposits and withdrawals;

- transfer initiated by telephones;

- debit cards;

- blink credit cards (contactless payment system);

- smart cards;

- mobile digital wallets; and

- wire transfer by Society for Worldwide Interbank Financial Telecommunication (SWIFT).

Pension services: Most banks assist customers in establishing retirement savings plans. Banks serve as financial intermediaries by receiving funds and investing them as directed by the customers and discussing investment options with customers.

Trust services: Banks manage funds left in a bank’s trust. For a fee they manage investment portfolio and estates of deceased persons.

Financial advice: Banks advise their customers about investment opportunities and options. Banks stress their role as financial advisors.

International services: International services that banks provide include: currency exchange, letters of credit and bankers’ acceptances.

You can appreciate the diversity of the services offered by chartered banks by visiting their Web sites. For example, Royal Bank of Canada (RBC) promotes services to four categories of customers: individuals, small businesses, corporate and institutional clients, and affluent clients seeking wealth management. In addition to traditional chequing and savings accounts, the bank offers automated teller machine (ATM) services, credit cards, and debit cards. It lends money for homes, cars, college, and other personal and business needs. It provides financial advice and sells securities and other financial products, including Registered Retirement Savings Plans (RRSPs), by which investors can save money that is tax free until they retire. RBC even offers life, auto, disability, and homeowners’ insurance. It also provides electronic banking for customers who want to check balances, transfer funds, and pay bills online.[4]

How Banks Expand the Money Supply

When you deposit money, your bank does not set aside a special pile of cash with your name on it. It merely records the fact that you made a deposit and increases the balance in your account. Depending on the type of account, you can withdraw your share whenever you want, but until then, it is added to all the other money held by the bank. Because the bank can be pretty sure that all its depositors would not withdraw their money at the same time, it holds onto only a fraction of the money that it takes in — its reserves. It lends out the rest to individuals, businesses, and the government, earning interest income and expanding the money supply.

The Role of the Bank of Canada

The Bank of Canada is the nation’s central bank. Its principal role is “to promote the economic and financial welfare of Canada,” as defined in the Bank of Canada Act. The Bank of Canada is a special type of Crown corporation that is owned by the federal government, but has considerable independence to carry out its responsibilities and therefore operates separately from the political process.

The Bank’s four main areas of responsibility are:[5]

- Monetary policy: The Bank influences the supply of money circulating in the economy, using its monetary policy framework to keep inflation low and stable.

- Financial systems: The Bank promotes safe, sound and efficient financial systems, within Canada and internationally, and conducts transactions in financial markets in support of these objectives.

- Currency: The Bank designs, issues and distributes Canada’s bank notes.

- Funds management: The Bank is the fiscal agent for the Government of Canada, managing its public debt programs and foreign exchange reserves.

The Bank of Canada is led by the Governing Council, the policy-making body of the Bank, which is responsible for:

- conducting monetary policy; and

- promoting a safe and efficient financial system.

The Governing Council is made up of the Governor, the Senior Deputy Governor and the Deputy Governors. The Governing Council’s main tool for conducting monetary policy is the target for the overnight rate (also known as the key policy rate). This rate is normally set on eight fixed announcement dates per year. The Council reaches its decisions about the rate by consensus, rather than by individual votes, as is the case at some other central banks.

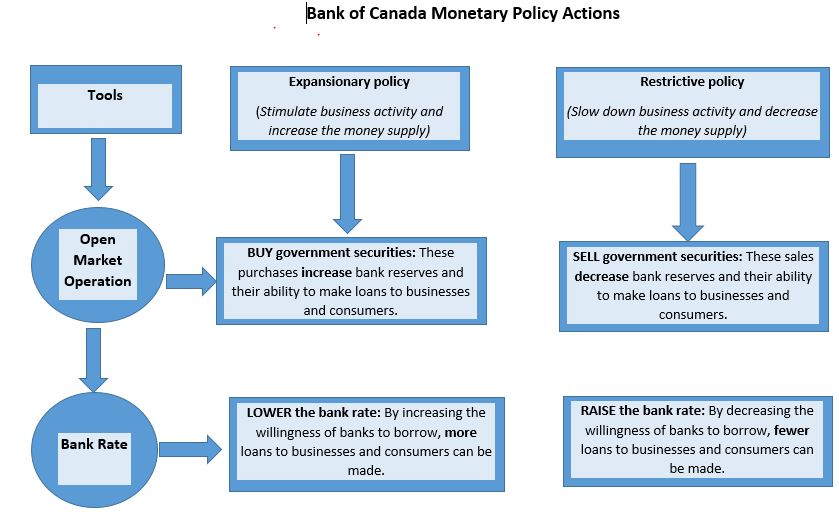

The Bank of Canada’s Role in Managing the Money Supply.

The Bank of Canada plays a vital role in managing the money supply in Canada. If the Bank of Canada wants to increase the money supply, it can buy government securities. The individuals and investors who sell these bonds then deposit the proceeds in their banks. These deposits increase banks’ reserves and their willingness to make loans. The Bank of Canada can also lower the bank rate; this action will cause increased demand for loans from businesses and households because these customers borrow more money when interest rates drop.

If the Bank of Canada wants to decrease the money supply, it can sell government securities. Individuals and investors spend money to buy bonds, and these withdrawals bring down banks’ reserves and reduce their willingness to make loans. The Bank of Canada can also raise the bank rate; this action will decrease the demand for loans from businesses and households because these customers borrow less money when interest rates rise.

Exhibit 2: Illustrations of Bank of Canada monetary policy actions.

Alternate Banks

The big banks — Chartered Banks — in Canada, including BMO, CIBC, RBC, Scotiabank, and TD, offer a large variety of banking products. Alternate banks are Credit Unions, Trust companies and Online Banks that specialize and tend to offer better rates and lower fees.

Credit Unions

Credit unions are cooperative savings, owned by their members with common interest, who receive shares of their profits. They offer almost anything that a chartered bank offers — savings account and loans, chequing accounts, home and car loans, credit cards, and even some commercial loans.

Trust Companies

A trust company safeguards property — funds and estates — entrusted to it. It may serve as a trustee, transfer agent, and registrar for corporations, and provide other services as well. In recent years trust companies have declined in importance.

Online Banks

Due to the global pandemic over the past year and a half, we have seen just how little we rely on in-person services from brick-and-mortar banks, with most people avoiding their local branch and opting to use online products offered by their traditional banks instead.

The online banking industry in Canada got its start around 1996, and although people were somewhat skeptical at first, the industry has grown to proportions today that rival the traditional banking industry.

Online banks have significant advantages over their traditional counterparts. They have developed a business model that provides customers with the best of both worlds: low — and even no — monthly fees, along with accessible customer service administered remotely. Examples in Canada include: Tangerine, EQ Bank, Neo Financial, Simplii Financial and Manulife Bank.

Specialized Lending and Savings Intermediaries

Finance Companies or Financial Corporation

Finance companies are non-deposit institutions because they do not accept deposits from individuals or provide traditional banking services, such as chequing accounts. They do, however, make loans to individuals and businesses, using funds acquired by selling securities or borrowed from chartered banks. Those that lend money to businesses, such as General Electric Capital Corporation, are commercial finance companies, and those that make loans to individuals or issue credit cards, such a PCFinancial are consumer finance companies. Some, such as General Motors Acceptance Corporation, provide loans to both consumers (car buyers) and businesses (GM dealers).

Insurance Companies

Insurance companies sell protection against losses incurred by illness, disability, death, and property damage. To finance claims payments, they collect premiums from policyholders, which they invest in stocks, bonds, and other assets. They also use a portion of their funds to make loans to individuals, businesses, and government agencies. Manulife is the leading Canadian life insurance company, and it has an international presence.

Brokerage Firms or Factoring Companies

Companies like Commercial Capital LLC, who buy and sell stocks, bonds, and other investments for clients, are brokerage firms (also called securities investment dealers). A mutual fund invests money from a pool of investors in stocks, bonds, and other securities. Investors become part owners of the fund. Mutual funds reduce risk by diversifying investment; because assets are invested in dozens of companies in a variety of industries, poor performance by some firms is usually offset by good performance by others. Mutual funds may be stock funds, bond funds, and money market funds, which invest in safe, highly liquid securities.

Finally, pension funds, which manage contributions made by participating employees and employers and provide members with retirement income, are also non-deposit institutions.

Venture Capital Firms

Venture Capital Firms provide private equity financing or funds to start-ups, early-stage, and emerging companies that have been deemed to have high growth potential or that have demonstrated high growth. Venture capital generally comes from wealthy investors, investment banks, and any other financial institutions. However, it does not always take a monetary form; it can also be provided in the form of technical or managerial expertise. Financing new and untested venture can be risky for investors who put up funds, however, the potential for above-average returns is an attractive payoff.

Pension Funds

A pension fund is any plan, fund, or scheme that provides retirement income in the future to subscribers. Pension funds typically have large amounts of money to invest and are the major investors in listed and private companies.

Other Sources of Funds

Government Financial Institutions and Granting Agencies

The Canadian government provides government funding support to businesses across the country. This funding support comes in the form of government grants, government loans, tax breaks, tax credits and other types of financial contributions. A number of provincial agencies also provide funding to developing business firms in the hope that they will provide jobs in the province. There are both federal and provincial programs supporting the agriculture industry and providing grants to business operations.

Some examples of federal agencies include:

- The Business Development Bank of Canada (BDC) makes term loans, primarily to smaller firms judged to have growth potential but unable to secure funds at reasonable terms from traditional sources. They also provide counselling services to support their clients.

- The federal government’s Export Development Corporation (EDC) finances and insures export sales for Canadian companies.

- The Canada Mortgage and Housing Corporation(CMHC) is involved in providing and guaranteeing mortgages. The CMHC is important to the construction industry.

- Crown-Indigenous Relations and Northern Affairs Canada (CIRNAC) and Indigenous Services Canada (ISC) provide numerous services to First Nations or Indigenous peoples.

- Futurpreneur Canada is a non-profit organization helping Canadians aged 18-39 become business owners with loan financing, mentoring and business resources.

International Banking and Finance

Foreign sources of funds have been important throughout the economic development of Canada. The Canadian capital market is one part of the international capital market. Canadian provinces borrow in foreign markets such as London and New York. Future projections of Canadian capital requirements indicate that organizations will continue to need these funds.

What roles do Canadian banks play in the international marketplace?

The financial marketplace spans the globe, with money routinely flowing across international borders. Canadian banks play an important role in global business by providing loans to foreign governments and businesses. Multinational corporations need many special banking services, such as foreign currency exchange and funding for overseas investments. Canadian banks also offer trade-related services, such as global cash management, that help firms manage their cash flow, improve their payment efficiency, and reduce their exposure to operational risks. Sometimes consumers in other nations have a need for banking services that banks in their own countries do not provide. Therefore, large banks often look beyond their national borders for profitable banking opportunities.

Some Canadian banks have expanded into overseas markets by opening offices in Europe, Latin America, and Asia. They often provide better customer service than local banks and have access to more sources of funding.

For Canadian banks, expanding internationally can be difficult. Banks in other nations are often subject to fewer regulations than Canadian banks, making it easier for them to undercut Canadian banks on the pricing of loans and services. Some governments also protect their banks against foreign competition. For example, the Chinese government imposes high fees and limits the amount of deposits that foreign banks can accept from customers. It also controls foreign bank deposits and loan interest rates, limiting the ability of foreign banks to compete with government-owned Chinese banks. Despite the banking restrictions for foreign banks in China, some Canadian banking institutions continue to do business there.[6]

International banks operating within Canada have a substantial impact on the economy through job creation — they employ thousands of people in Canada, and most workers are Canadian citizens — operating and capital expenditures, taxes, and other contributions.

Political and economic uncertainty in other countries can make international banking a high-risk venture. European and Asian banks were not immune to the financial crisis of 2007–2009. In fact, several countries, including Greece, Portugal, Spain, and Ireland, continue to rebound slowly from the near-collapse of their economic and financial systems that they experienced a decade ago. Financial bailouts spearheaded by the European Union and the International Monetary Fund have helped stabilize the European and global economy.

Currency Values and Exchange Rates

Currencies are traded in the foreign exchange market. Like any other market, when something is exchanged there is a price. In the foreign exchange market, a currency is being bought and sold, and the price of that currency is given in some other currency. That price is expressed as an exchange rate.

When an exchange rate changes, the value of one currency will go up while the value of the other currency will go down. When the value of a currency increases, it is said to have appreciated. On the other hand, when the value of a currency decreases, it is said to have depreciated.

The Canadian dollar fluctuates against the American dollar between 65-70 per cent range. On November 2007, the CAD dollar was stronger than the US dollar, at US $1.09. After a few years of parity, the Canadian dollar retreated to approximately US $0.76 in June 2018.[7] These fluctuations have an impact on businesses.

International Payment Process

International financial settlements between buyers and sellers are different in many countries. Canadian banks provide services to buyers and sellers to support their clients during global financial transactions. Country-to-country transactions rely on an international payment process that moves money between buyers and sellers in different countries. For example, payment from a Canadian buyer start at a local bank that converts funds from dollars into the seller’s currency, say British pounds sterling, to be sent to a seller in England. At the same time, payments and currency conversions from separate transactions are also flowing between British businesses and Canadian sellers in the other direction. A balance trade between the two countries implies that money inflows and outflows are equal for both countries. If inflows and outflows are not in balance at the Canadian bank or the British bank, then a flow of money — either to England or Canada — is made to cover the difference.

International Banking Structure – World Bank and International Monetary Fund

Policymaking and regulatory powers are different in every nation; local standards and laws also vary greatly, which means that banking systems vary greatly. These two United Nation agencies — The World Bank and International Monetary Fund — assist in financing international trade.

The World Bank

The World Bank is an important source of economic assistance for poor and developing countries. With backing from wealthy donor countries (such as Canada, the United States, Japan, Germany, and the United Kingdom), the World Bank provides loans, grants, and guarantees to some of the world’s poorest nations. Loans are made to help countries improve the lives of the poor through community support programs designed to provide health, nutrition, education, infrastructure, and other social services.

The International Monetary Fund

The International Monetary Fund (IMF) consists of 189 nations who, as a group, combine their resources to:

- encourage the development of a system for international payments;

- promote the stability of exchange rates;

- provide temporary, short term loans to member countries; and

- encourage members to cooperate on international monetary issues.

The IMF loans money to countries with troubled economies, such as Mexico in the 1980s and mid-1990s, and Russia and Argentina in the late 1990s. There are, however, strings attached to IMF loans; in exchange for relief in times of financial crisis, borrower countries must institute sometimes painful financial and economic reforms. In the 1980s, for example, Mexico received financial relief from the IMF on the condition that it privatize and deregulate certain industries and liberalize trade policies. The government was also required to cut back expenditures for such services as education, health care, and workers’ benefits.

Some nations have declined IMF funds rather than accept the economic changes that the IMF demands. In 2021, according to the IMF website, the IMF had about $1 trillion available for loans. Despite the fact that the U.S. has been instrumental in promoting global free trade for decades in 2018, it was rumoured that under Trump’s administration the U.S. would withdraw from the World Trade Organization (WTO). This did not happen but the instability caused by such news was damaging to the WTO.

Digital Currencies

Digital currencies are currencies that are only accessible with computers or mobile phones because they only exist in electronic form. Digital money is not physically tangible like a dollar bill or a coin. It is accounted for and transferred using online systems. The difference between digital currencies and cryptocurrencies is that digital currencies are centralized, meaning that transaction within the network is regulated in a centralized location, like a bank. Cryptocurrencies are mostly decentralized, and the regulations inside the network are governed by the majority of the community.

The Bank of Canada revealed in 2016 that it was developing the CAD-coin as a digital version of the Canadian dollar, a move in response to the rise in popularity of bitcoin and other blockchain-based digital currencies. The initiative will involve issuing, transferring and settling the central bank’s monetary assets by way of a computerized ledger rather than by way of printed dollars. Research and experiments have been ongoing since 2016. Some major banks in Canada are participating in this new initiative, including Royal Bank of Canada, CIBC and TD Bank Group, and institutional partners such as Payments Canada and TMX Group.

Despite their claim of being the money of the future, current private digital currencies, like bitcoin, do not work well for making payments or saving for the future. Because of their fluctuating values and slow clearing times, very few merchants accept them. It is possible that in the future digital currencies could at least partially solve these problems, leading to greater adoption. But widespread adoption of private digital currencies would carry important risks to both the economy and the financial system. The issuer could go out of business or fall victim to cybertheft; either situation could cause a loss of confidence in the payment system.

Exploring the idea of a central bank digital currency makes sense. In theory, it could provide the safety of cash, with the convenience of modern electronic payments. It could take many forms, but two broad approaches are:

- value-based — people transfer money from their bank account to a card or a phone app; or

- account-based — people or businesses open accounts at the central bank.

Either way, payments made using a central bank digital currency could allow payments to remain private to the parties involved, just like cash but

Central bank digital currencies could give consumers more choice while maintaining competition among financial service providers like banks, the way cash does now. Depending on their design, they could even act as a backup if other payment methods become temporarily unavailable.

Basically, central bank digital cash would act like current electronic payment methods, the only difference being that it would not be tied to a commercial bank the way bank accounts and debit cards are.[8]

Comprehensive Check

- Define the following terms:

- money;

- M1 and M2 money supply;

- electronic funds transfer (EFT); and

- digital currency.

- What are the crucial properties of money?

- What services do financial institutions provide in Canada?

- List the functions of the Bank of Canada.

- Explain the balance of trade between two nations.

Key Takeaways

- Money serves three basic functions:

- Medium of exchange: because you can use it to buy the goods and services you want, everyone’s willing to trade things for money.

- Measure of value: it simplifies the exchange process because it’s a means of indicating how much something costs.

- Store of value: people are willing to hold onto it because they’re confident that it will keep its value over time.

- The government uses two measures to track the money supply: M-1 includes the most liquid forms of money, such as cash and chequing account funds. M-2 includes everything in M-1 plus near-cash items, such as savings accounts and term deposits below $100,000.

- Financial institutions serve as financial intermediaries between savers and borrowers and direct the flow of funds between the two groups.

- Those that accept deposits from customers — depository institutions (chartered banks) — include commercial banks, savings banks, and credit unions; those that do not — non-depository institutions — include finance companies, insurance companies, and brokerage firms (investment dealers).

- Financial institutions offer a wide range of services, including checking and savings accounts, ATM services, and credit and debit cards. They also sell securities and provide financial advice.

- A bank holds onto only a fraction of the money that it takes in — an amount called its reserves — and lends the rest out to individuals, businesses, and governments. In turn, borrowers put some of these funds back into the banking system, where they become available to other borrowers. The money multiplier effect ensures that the cycle expands the money supply.

- Currency — paper money (bills) and coins issued by the Canadian government.

- Credit card — immediately transfers money from the credit card company’s chequing account to the seller, and at the end of the month the user owes the money to the credit card company; a credit card is a short-term loan.

- Debit card — like a cheque, is an instruction to the bank to transfer money directly and immediately from the user’s bank account to the seller.

- Demand deposit — chequable deposit in banks that is available by making a cash withdrawal or writing a cheque.

- M1 money supply — a narrow definition of the money supply that includes currency and chequing accounts in banks, and to a lesser degree, traveler’s cheques.

- M2 money supply — a definition of the money supply that includes everything in M1, but also adds savings deposits, money market funds, and certificates of deposit.

- Money market mutual funds — the deposits of many investors are pooled together and invested in a safe way, like short-term government bonds and other low-risk financial securities.

- Savings deposit — bank account from which the user cannot withdraw money by writing a cheque, but can withdraw the money at a bank — or can transfer it easily to a chequing account.

- Smart card — stores a certain value of money on a card with which the user can make purchases.

- Time deposit — an account that the depositor has committed to leaving in the bank for a certain period of time, in exchange for a higher rate of interest; also called certificate of deposit. Requires prior notice of withdrawal and cannot be transferred by cheque.

- International Banking and Finance — changes in currency values and exchange rates reflect global supply and demand for various currencies. Central Banks’ policies on money supplies and interest rates influence the value of currencies in the foreign currency/exchange markets.

- The World Bank and International Monetary fund provide stability to encourage international trade.

- Digital currency (digital money, electronic money or electronic currency) is primarily managed, stored or exchanged on digital computer systems, especially over the internet.

Attributions

This Chapter is adapted from Introduction to Business — licensed under a Creative Commons Attribution 4.0 International CC BY-NC-SA (Attribution NonCommercial ShareAlike) license, which means that you can distribute, remix, and build upon the content, as long as you provide attribution to OpenStax and its content contributors. The chapter differs from the original to reflect Canadian content.

The section on the Functions of Money is adapted from Exploring Business and is adapted from a work produced and distributed under a Creative Commons license (CC BY-NC-SA) in 2010 by a publisher who has requested that they and the original author not receive attribution. This adapted edition is produced by the University of Minnesota Libraries Publishing through the eLearning Support Initiative.

Image – Measuring the Money Supply M1-M2 from Open textbook Principles of Economics

- Statistics Canada. (2018, March 14). Currency composition of Canada’s international investment position. https://www150.statcan.gc.ca/n1/pub/13-605-x/2018001/article/54916-eng.htm ↵

- Trading Economics. (n.d.). Canada Money Supply M2. https://tradingeconomics.com/canada/money-supply-m2 ↵

- Statistics Canada. (n.d.). Table 10-10-0109-01 Chartered banks, assets and liabilities, month-end, Bank of Canada (x 1,000,000). https://doi.org/10.25318/1010010901-eng ↵

- Royal Bank of Canada. (n.d.). Our Company. https://www.rbc.com/our-company/index.html ↵

- Bank of Canada. (n.d.). About Us. https://www.bankofcanada.ca/about/ ↵

- Bank of Montreal Canada. (n.d.). About BMO ChinaCo. https://www.bmo.com/asia/about_BMO_China.html ↵

- Xe. (n.d.). US Dollar to Canadian Dollar Exchange Rate Chart. https://www.xe.com/currencycharts/?from=USD&to=CAD ↵

- Bank of Canada. (n.d.). The Road to Digital Money. https://www.bankofcanada.ca/2019/04/the-road-to-digital-money/ ↵

Key terms appear throughout the chapter. When you click on them, a definition will pop up. If you are using a downloaded or printed format, check the glossary in the back of the book. Please make sure you can define them!

Money is a medium of exchange, serves as a measure of value and a store of value.

Electronic funds transfer (EFT) is the electronic transfer of money from one bank account to another, either within a single financial institution or across multiple institutions, via computer-based systems, telephones without the direct intervention of bank staff.