Part C – Understanding the Business of Managing

Chapter 17 – Financial Decisions and Risk Management

Learning Objectives

By the end of the chapter, you should be able to:

- explain how financial decisions affect the overall business strategy;

- discuss the role and responsibilities of the financial manager;

- distinguish between short-term (operating) and long-term (capital) expenditures;

- explain the ways in which a new business gets start-up cash;

- identify approaches used by existing companies to finance operations and growth;

- identify sources of short-term and long-term financing for business;

- distinguish between equity and debt financing;

- explain the process by which securities are bought and sold and describe the secondary market for each type of security;

- describe the investment opportunities offered by mutual funds, exchange traded funds, hedge funds, and commodities;

- explain how risk affects business operations and identify the five steps in the risk management process; and

- explain key terms in the chapter.

Show What You Know

Show What You Know

How Do Finance and the Financial Manager affect the Business’s Overall Strategy?

Any company, whether it is a small town bakery or Tim Hortons, needs money to operate. To make money, it must first spend money — on inventory and supplies, equipment and facilities, and employee wages and salaries. Therefore, finance is critical to the success of all companies. It may not be as visible as marketing or production, but management of a firm’s finances is just as key to the firm’s success.

Financial management — the art and science of managing a firm’s money so that it can meet its goals — is not just the responsibility of the finance department. All business decisions have financial consequences. Managers in all departments must work closely with financial personnel. If you are a sales representative, for example, the company’s credit and collection policies will affect your ability to make sales. The head of the IT department will need to justify any requests for new computer systems or employee laptops.

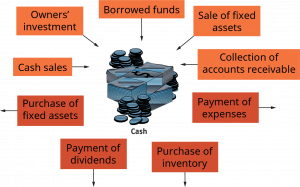

Revenue from sales of the firm’s products should be the chief source of funding. But money from sales does not always come in when it is needed to pay the bills. Financial managers must track how money is flowing into and out of the firm (see Exhibit 17.1). They work with the firm’s other department managers to determine how available funds will be used and how much money is needed. Then they choose the best sources to obtain the required funding.

For example, a financial manager will track day-to-day operational data such as cash collections and disbursements to ensure that the company has enough cash to meet its obligations. Over a longer time horizon, the manager will thoroughly study whether and when the company should open a new manufacturing facility. The manager will also suggest the most appropriate way to finance the project, raise the funds, and then monitor the project’s implementation and operation.

Financial management is closely related to accounting. In most firms, both areas are the responsibility of the vice president of finance or CFO. But the accountant’s main function is to collect and present financial data. Financial managers use financial statements and other information prepared by accountants to make financial decisions. Financial managers focus on cash flows, the inflows and outflows of cash. They plan and monitor the firm’s cash flows to ensure that cash is available when needed.

The Financial Manager’s Responsibilities and Activities

Financial managers have a complex and challenging job. They analyze financial data prepared by accountants, monitor the firm’s financial status, and prepare and implement financial plans. One day they may be developing a better way to automate cash collections, and the next they may be analyzing a proposed acquisition. The key activities of the financial manager are:[1]

- Financial planning: preparing the financial plan, which projects revenues, expenditures, and financing needs over a given period;

- Investment (spending money): investing the firm’s funds in projects and securities that provide high returns in relation to their risks;

- Financing (raising money): obtaining funding for the firm’s operations and investments and seeking the best balance between debt (borrowed funds) and equity (funds raised through the sale of ownership in the business); and

- Financial Control: checking performance against strategic plans.

The Goal of the Financial Manager

How can financial managers make wise planning, investment, and financing decisions? The main goal of the financial manager is to maximize the value of the firm to its owners. The value of a publicly owned corporation is measured by the share price of its stock. A private company’s value is the price at which it could be sold.

To maximize the firm’s value, the financial manager has to consider both short- and long-term consequences of the firm’s actions. Maximizing profits is one approach, but it should not be the only one. Such an approach favors making short-term gains over achieving long-term goals. What if a firm in a highly technical and competitive industry did no research and development? In the short run, profits would be high because research and development is very expensive. But in the long run, the firm might lose its ability to compete because of its lack of new products.

In finance, the opportunity for profit is called return; the potential for loss, or the chance that an investment will not achieve the expected level of return, is risk. A basic principle in finance is that the higher the risk, the greater the return that is required. This widely accepted concept is called the risk-return trade-off. Financial managers consider many risk and return factors when making investment and financing decisions. Among them are changing patterns of market demand, interest rates, general economic conditions, market conditions, and social issues (such as environmental effects and equal employment opportunity policies).

What Types of Short-term and Long-term Expenditures does a Firm make?

To grow and prosper, a firm must keep investing money in its operations. The financial manager decides how best to use the firm’s money. Short-term expenses support the firm’s day-to-day activities. For instance, athletic apparel maker lululemon Athletica regularly spends money to buy such raw materials as leather and fabric, and to pay employee salaries. Long-term expenses are typically for fixed assets. For lululemon, these would include outlays to build a new factory, buy automated manufacturing equipment, or acquire a small manufacturer of sports apparel.

Short-Term Expenses

Short-term expenses, often called operating expenses, are outlays used to support current production and selling activities. They typically result in current assets, which include cash and any other assets (accounts receivable and inventory) that can be converted to cash within a year. The financial manager’s goal is to manage current assets so the firm has enough cash to pay its bills and to support its accounts receivable and inventory.

Cash Management: Assuring Liquidity

Cash is the lifeblood of business. Without it, a firm could not operate. An important duty of the financial manager is cash management, or making sure that enough cash is on hand to pay bills as they come due and to meet unexpected expenses.

Businesses estimate their cash requirements for a specific period. Many companies keep a minimum cash balance to cover unexpected expenses or changes in projected cash flows. The financial manager arranges loans to cover any shortfalls. If the size and timing of cash inflows closely match the size and timing of cash outflows, the company needs to keep only a small amount of cash on hand. A company whose sales and receipts are fairly predictable and regular throughout the year needs less cash than a company with a seasonal pattern of sales and receipts. A toy company, for instance, whose sales are concentrated in the fall, spends a great deal of cash during the spring and summer to build inventory. It has excess cash during the winter and early spring, when it collects on sales from its peak selling season.

Because cash held in checking accounts earns little, if any, interest, the financial manager tries to keep cash balances low and to invest the surplus cash. Surpluses are invested temporarily in marketable securities, short-term investments that are easily converted into cash. The financial manager looks for low-risk investments that offer high returns. Four of the most popular marketable securities are Treasury bills, certificates of deposit, commercial paper, and banker’s acceptances. (Commercial paper is unsecured short-term debt — an IOU — issued by a financially strong corporation.)

A banker’s acceptance (BA) is a type of commercial paper; an unsecured short-term debt issued by a lesser financially strong corporation that is guaranteed by a bank for a fee. The bank guarantee makes the BA a secured note for the buyer.

Today’s financial managers have new tools to help them find the best short-term investments, such as online trading platforms that save time and provide access to more types of investments. These have been especially useful for smaller companies who don’t have large finance staffs.[2]

Companies with overseas operations face even greater cash management challenges. Developing the systems for international cash management may sound simple in theory, but in practice it’s extremely complex. In addition to dealing with multiple foreign currencies, treasurers must understand and follow banking practices and regulatory and tax requirements in each country. Regulations may impede their ability to move funds freely across borders. Also, issuing a standard set of procedures for every office may not work because local business practices differ from country to country. In addition, local managers may resist the shift to a centralized structure because they don’t want to give up control of cash generated by their units. Corporate financial managers must be sensitive to and aware of local customs and adapt the centralization strategy accordingly.

In addition to seeking the right balance between cash and marketable securities, the financial manager tries to shorten the time between the purchase of inventory or services (cash outflows) and the collection of cash from sales (cash inflows). The three key strategies are to collect money owed to the firm (accounts receivable) as quickly as possible, to pay money owed to others (accounts payable) as late as possible without damaging the firm’s credit reputation, and to minimize the funds tied up in inventory.

Managing Accounts Receivable

Accounts receivable represent sales for which the firm has not yet been paid. Because the product has been sold but cash has not yet been received, an account receivable amounts to a use of funds. For the average manufacturing firm, accounts receivable represent about 15 to 20 percent of total assets.

The financial manager’s goal is to collect money owed to the firm as quickly as possible, while offering customers credit terms attractive enough to increase sales. Accounts receivable management involves setting credit policies, guidelines on offering credit, credit terms, and specific repayment conditions, including how long customers have to pay their bills and whether a cash discount is given for quicker payment. Another aspect of accounts receivable management is deciding on collection policies, the procedures for collecting overdue accounts.

Setting up credit and collection policies is a balancing act for financial managers. On the one hand, easier credit policies or generous credit terms (a longer repayment period or larger cash discount) result in increased sales. On the other hand, the firm has to finance more accounts receivable. The risk of uncollectible accounts receivable also rises. Businesses consider the impact on sales, timing of cash flow, experience with bad debt, customer profiles, and industry standards when developing their credit and collection policies.

Companies that want to speed up collections actively manage their accounts receivable, rather than passively letting customers pay when they want to. Many businesses experience late payments from customers, and some companies write off a percentage of their bad debt, which can be expensive.

Technology plays a big role in helping companies improve their credit and collections performance. For example, many companies use some type of automated decision making, whether that comes in the form of an Enterprise Relational Planning (ERP) system or a combination of software programs and supplemental modules that help companies make informed decisions when it comes to credit and collection processes.[3]

Other companies choose to outsource financial and accounting business processes to specialists rather than develop their own systems. The availability of cutting-edge technology and specialized electronic platforms that would be difficult and expensive to develop in-house is winning over firms of all sizes. Giving up control of finance to a third party has not been easy for CFOs. The risks are high when financial and other sensitive corporate data are transferred to an outside computer system: data could be compromised or lost, or rivals could steal corporate data. It’s also harder to monitor an outside provider than your own employees. One outsourcing area that has attracted many clients is international trade, which has regulations that differ from country to country and requires huge amounts of documentation. With specialized IT systems, providers can track not only the physical location of goods, but also all the paperwork associated with shipments. Processing costs for goods purchased overseas are about twice those of domestic goods, so more efficient systems pay off.[4]

Inventory

Another use of funds is to buy inventory needed by the firm. In a typical manufacturing firm, inventory comprises nearly 20 percent of total assets. The cost of inventory includes not only its purchase price, but also ordering, handling, storage, interest, and insurance costs.

Production, marketing, and finance managers usually have differing views about inventory. Production managers want lots of raw materials on hand to avoid production delays. Marketing managers want lots of finished goods on hand so customer orders can be filled quickly. But financial managers want the least inventory possible without harming production efficiency or sales. Financial managers must work closely with production and marketing to balance these conflicting goals. Techniques for reducing the investment in inventory are inventory management, the just-in-time (JIT) system, and materials requirement planning.

For retail firms, inventory management is a critical area for financial managers, who closely monitor inventory turnover ratios. This ratio shows how quickly inventory moves through the firm and is turned into sales. If the inventory number is too high, it will typically affect the amount of working capital a company has on hand, forcing the company to borrow money to cover the excess inventory. If the turnover ratio number is too high, it means the company does not have enough inventory of products on hand to satisfy customer needs, which means they could take their business elsewhere.

Long-Term Expenditures

A firm also invests funds in physical assets such as land, buildings, machinery, equipment, and information systems. These are called capital expenditures. Unlike operating expenses, which produce benefits within a year, the benefits from capital expenditures extend beyond one year. For instance, a printer’s purchase of a new printing press with a usable life of seven years is a capital expenditure and appears as a fixed asset on the firm’s balance sheet. Paper, ink, and other supplies, however, are expenses. Mergers and acquisitions are also considered capital expenditures.

Firms make capital expenditures for many reasons. The most common are to expand, to replace or renew fixed assets, and to develop new products. Most manufacturing firms have a big investment in long-term assets. Boeing Company, for instance, puts billions of dollars a year into airplane manufacturing facilities. Because capital expenditures tend to be costly and have a major effect on the firm’s future, the financial manager uses a process called capital budgeting to analyze long-term projects and select those that offer the best returns while maximizing the firm’s value. Decisions involving new products or the acquisition of another business are especially important. Managers look at project costs and forecast the future benefits the project will bring to calculate the firm’s estimated return on the investment.

Sources and Costs of Secured and Unsecured Short-term Financing?

How do firms raise the funding they need? They borrow money (debt), sell ownership shares (equity), and retain earnings (profits). The financial manager must assess all these sources and choose the one most likely to help maximize the firm’s value.

Like expenses, borrowed funds can be divided into short- and long-term loans. A short-term loan comes due within one year; a long-term loan has a maturity greater than one year. Short-term financing is shown as a current liability on the balance sheet and is used to finance current assets and support operations. Short-term loans can be unsecured or secured.

Unsecured Short-Term Loans

Unsecured loans are made on the basis of the firm’s creditworthiness and the lender’s previous experience with the firm. An unsecured borrower does not have to pledge specific assets as security. The four main types of unsecured short-term loans are trade credit, bank loans, banker’s acceptances (BA’s) and commercial paper.

Trade Credit: Accounts Payable

When Goodyear sells tires to General Motors Canada (GMC), GMC does not have to pay cash on delivery. Instead, Goodyear regularly bills GMC for its tire purchases, and GMC pays at a later date. This is an example of trade credit: the seller extends credit to the buyer between the time the buyer receives the goods or services and when it pays for them. Trade credit is a major source of short-term business financing. The buyer enters the credit on its books as an account payable. In effect, the credit is a short-term loan from the seller to the buyer of the goods and services. Until GMC pays Goodyear, Goodyear has an account receivable from GMC, and GMC has an account payable to Goodyear.

Bank Loans

Unsecured bank loans are another source of short-term business financing. Companies often use these loans to finance seasonal (cyclical) businesses. Unsecured bank loans include lines of credit and revolving credit agreements. A line of credit specifies the maximum amount of unsecured short-term borrowing the bank will allow the firm over a given period, typically one year. The firm either pays a fee or keeps a certain percentage of the loan amount (generally 10 to 20 percent) in a checking account at the bank. Another bank loan, the revolving credit agreement, is basically a guaranteed line of credit that carries an extra fee in addition to interest. Revolving credit agreements are often arranged for a period of two to five years.

Commercial Paper Bankers Acceptances

As noted earlier, commercial paper is an unsecured short-term debt — an IOU — issued by a financially strong corporation. Thus, it is both a short-term investment and a financing option for major corporations. Corporations issue commercial paper in multiples of $100,000 for periods ranging from 3 to 270 days. Many big companies use commercial paper instead of short-term bank loans because the interest rate on commercial paper is usually 1 to 3 percent below bank rates.

Secured Short-Term Loans

Secured loans require the borrower to pledge specific assets as collateral, or security. The secured lender can legally take the collateral if the borrower doesn’t repay the loan. Commercial banks and commercial finance companies are the main sources of secured short-term loans to business. Borrowers whose credit is not strong enough to qualify for unsecured loans use these loans. Typically, the collateral for secured short-term loans is accounts receivable or inventory. Because accounts receivable are normally quite liquid (easily converted to cash), they are an attractive form of collateral. The appeal of inventory — raw materials or finished goods — as collateral depends on how easily it can be sold at a fair price. Note the collateral is checked regularly to ensure it exists. If it has been sold without the lender’s knowledge it is an illegal activity referred to as “fraudulent conversion.”

Another form of short-term financing using accounts receivable is factoring. A firm sells its accounts receivable outright to a factor, a financial institution (often a commercial bank or commercial finance company) that buys accounts receivable at a discount. Factoring is widely used in the clothing, furniture, and appliance industries. Factoring is more expensive than a bank loan, however, because the factor buys the receivables at a discount from their actual value.

For businesses with steady orders but a lack of cash to make payroll or other immediate payments, factoring is a popular way to obtain financing. In factoring, a company sells its invoices to a third-party funding source for cash. The factor purchasing the invoices then collects on the due payments over time. Trucking companies with voluminous accounts receivable in the form of freight bills are good candidates for the use of short-term financing such as factoring.

Key Differences between Debt and Equity

A basic principle of finance is to match the term of the financing to the period over which benefits are expected to be received from the associated outlay. Short-term items should be financed with short-term funds, and long-term items should be financed with long-term funds. Long-term financing sources include both debt (borrowing) and equity (ownership). Equity financing comes either from selling new ownership interests or from retaining earnings. Financial managers try to select the mix of long-term debt and equity that results in the best balance between cost and risk.

Debt versus Equity Financing

Say that Bombardier Inc. plans to spend $2 billion over the next four years to build and equip new factories to make jet aircraft. Bombardier Inc.’s top management will assess the pros and cons of both debt and equity and then consider several possible sources of the desired form of long-term financing.

The major advantage of debt financing is the deductibility of interest expense for income tax purposes, which lowers its overall cost. In addition, there is no loss of ownership. The major drawback is financial risk: the chance that the firm will be unable to make scheduled interest and principal payments. The lender can force a borrower that fails to make scheduled debt payments into bankruptcy. Most loan agreements have restrictions to ensure that the borrower operates efficiently.

Equity, on the other hand, is a form of permanent financing that places few restrictions on the firm. The firm is not required to pay dividends or repay the investment. However, equity financing gives common stockholders voting rights that provide them with a voice in management. Equity is more costly than debt. Unlike the interest on debt, dividends to owners are not tax-deductible expenses. Table 17.1 summarizes the major differences between debt and equity financing.

Debt Financing

Long-term debt is used to finance long-term (capital) expenditures. The initial maturities of long-term debt typically range between 5 and 20 years. Three important forms of long-term debt are term loans, bonds, and mortgage loans.

| Debt Financing | Equity Financing | |

|---|---|---|

| Have a say in management | Creditors typically have none, unless the borrower defaults on payments. Creditors may be able to place restraints on management in event of default. | Common stockholders have voting rights. |

| Have a right to income and assets | Debt holders rank ahead of equity holders. Payment of interest and principal is a contractual obligation of the firm. | Equity owners have a residual claim on income (dividends are paid only after paying interest and any scheduled principal) and no obligation to pay dividends. |

| Maturity (date when debt needs to be paid back) | Debt has a stated maturity and requires repayment of principal by a specified date. | The company is not required to repay equity, which has no maturity date. |

| Tax treatment | Interest is a tax-deductible expense. | Dividends are not tax-deductible and are paid from after-tax income. |

A term loan is a business loan with a maturity of more than one year. Term loans generally have maturities of 5 to 12 years and can be unsecured or secured. They are available from commercial banks, insurance companies, pension funds, commercial finance companies, and manufacturers’ financing subsidiaries. A contract between the borrower and the lender spells out the amount and maturity of the loan, the interest rate, payment dates, the purpose of the loan, and other provisions such as operating and financial restrictions on the borrower to control the risk of default. The payments include both interest and principal, so the loan balance declines over time. Borrowers try to arrange a repayment schedule that matches the forecast cash flow from the project being financed.

Bonds are long-term debt obligations (liabilities) of corporations and governments. A bond certificate is issued as proof of the obligation. The issuer of a bond must pay the buyer a fixed amount of money — called interest, stated as the coupon rate — on a regular schedule, typically every six months. The issuer must also pay the bondholder the amount borrowed — called the principal, or par value — at the bond’s maturity date (due date). Bonds are usually issued in units of $1,000 — for instance, $1,000, $5,000, or $10,000 — and have initial maturities of 10 to 30 years. They are secured with specific collateral. If unsecured (no collateral) they are called debentures. Bonds and debentures may include special provisions for early retirement, or be convertible to common stock.

A mortgage loan is a long-term loan made against real estate as collateral. The lender takes a mortgage on the property, which lets the lender seize the property, sell it, and use the proceeds to pay off the loan if the borrower fails to make the scheduled payments. Long-term mortgage loans are often used to finance office buildings, factories, and warehouses. Life insurance companies are an important source of these loans. They make billions of dollars’ worth of mortgage loans to businesses each year.

Equity Financing and the Cost

Equity refers to the owners’ investment in the business. In corporations, the preferred and common stockholders are the owners. A firm obtains equity financing by selling new ownership shares (external financing) and by retaining earnings (internal financing). Small and growing, typically high-tech, companies, raise capital through venture capital firms (external financing) by giving up some ownership (i.e. selling shares).

Selling New Issues of Common Stock

Common stock is a security that represents an ownership interest in a corporation. A company’s first sale of stock to the public is called an initial public offering (IPO). An IPO often enables existing stockholders, usually employees, family, and friends who bought the stock privately, to earn big profits on their investment. (Companies that are already public can issue and sell additional shares of common stock to raise equity funds.)

But going public has some drawbacks. For one thing, there is no guarantee an IPO will sell. It is also expensive. Big fees must be paid to investment bankers, brokers, attorneys, accountants, and printers. Once the company is public, it is closely watched by regulators, stockholders, and securities analysts. The firm must reveal such information as operating and financial data, product details, financing plans, and operating strategies. Providing this information is often costly.

Going public is the dream of many small company founders and early investors, who hope to recoup their investments and become instant millionaires. Google went public in 2004 at $85 a share and soared to $475 in early 2006 before settling back to trade in the high-300 range in August 2006. More than a decade later, in October 2017, Google continues to be a successful IPO, trading at more than $990 per share.[5]

In recent years, the number of IPOs has dropped sharply, as start-ups think long and hard about going public, despite the promise of millions of dollars for investors and entrepreneurs. For example, in 2017, Blue Apron, a meal-kit delivery service, went public with an opening stock price of $10 per share. Several months later, the share price dropped more than 40 percent. Some analysts believe that Amazon’s possible entry into the meal-kit delivery sector has hurt Blue Apron’s value, as well as the company’s high marketing costs to attract and retain monthly subscribers.[6]

Some companies choose to remain private. Maple Leaf Sports & Entertainment, Mars Canada, London Drugs, Giant Tiger, Gateway Casinos, Harry Rosen Inc., Joe Fresh, and McCain Foods are among the largest Canadian private companies.

Spotify, the Swedish music streaming company went public on the New York Stock Exchange in April 2018. Instead of an initial public offering, Spotify opted for a direct listing, meaning rather than issue new shares, the company started trading by letting existing shareholders sell their shares directly on the public market. In doing so, Spotify pioneered the direct listing. It’s grown to 71 million paying subscribers and 159 million monthly active users. In the U.S., Spotify claims 41% of the U.S. market share, outpacing the reach of rival music services from Apple, Amazon, Pandora, Soundcloud and Tidal.[7]

Dividends and Retained Earnings

Dividends are payments to stockholders from a corporation’s profits. Dividends can be paid in cash or in stock. Stock dividends are payments in the form of more stock. Stock dividends may replace or supplement cash dividends. After a stock dividend has been paid, more shares have a claim on the same company, so the value of each share often declines. A company does not have to pay dividends to stockholders. But if investors buy the stock expecting to get dividends and the firm does not pay them, the investors may sell their stocks.

At their quarterly meetings, the company’s board of directors (typically with the advice of its CFO) decides how much of the profits to distribute as dividends and how much to reinvest. A firm’s basic approach to paying dividends can greatly affect its share price. A stable history of dividend payments indicates good financial health.

For example, the CIBC has increased its dividend more than 85% ($0.87 to $1.61) percent over the past ten years, giving shareholders a healthy return on their investment.[8]

If a firm that has been making regular dividend payments cuts or skips a dividend, investors start thinking it has serious financial problems. The increased uncertainty often results in lower stock prices. Thus, most firms set dividends at a level they can keep paying. They start with a relatively low dividend payout ratio so that they can maintain a steady or slightly increasing dividend over time.

Retained earnings, profits that have been reinvested in the firm, have a big advantage over other sources of equity capital: they do not incur underwriting costs. Financial managers strive to balance dividends and retained earnings to maximize the value of the firm. Often the balance reflects the nature of the firm and its industry. Well-established and stable firms and those that expect only modest growth, such as public utilities, financial services companies, and large industrial corporations, typically pay out much of their earnings in dividends.

Most high-growth companies, such as those in technology-related fields, finance much of their growth through retained earnings and pay little or no dividends to stockholders. As they mature, many decide to begin paying dividends, as Apple decided to do in 2012, after 17 years of paying no annual dividends to shareholders.[9]

Preferred Stock

Another form of equity is preferred stock. Unlike common stock, preferred stock usually has a dividend amount that is set at the time the stock is issued. These dividends must be paid before the company can pay any dividends to common stockholders. Also, if the firm goes bankrupt and sells its assets, preferred stockholders get their money back before common stockholders do.

Like debt, preferred stock increases the firm’s financial risk because it obligates the firm to make a fixed payment. But preferred stock is more flexible. The firm can miss a dividend payment without suffering the serious results of failing to pay back a debt.

Preferred stock is more expensive than debt financing, however, because preferred dividends are not tax-deductible. Also, because the claims of preferred stockholders on income and assets are second to those of debtholders, preferred stockholders require higher returns to compensate for the greater risk.

Venture Capital

Venture capital is another source of equity capital. It is most often used by small and growing firms that aren’t big enough to sell securities to the public. This type of financing is especially popular among high-tech companies that need large sums of money.

Venture capitalists invest in new businesses in return for part of the ownership, sometimes as much as 60 percent. They look for new businesses with high growth potential, and they expect a high investment return within 5 to 10 years. By getting in on the ground floor, venture capitalists buy stock at a very low price. They earn profits by selling the stock at a much higher price when the company goes public. Venture capitalists generally get a voice in management through seats on the board of directors. Getting venture capital is difficult, even though there are hundreds of private venture-capital firms in this country. Most venture capitalists finance only about 1 to 5 percent of the companies that apply. Venture-capital investors, many of whom experienced losses during recent years from their investments in failed dot-coms, are currently less willing to take risks on very early stage companies with unproven technology. As a result, other sources of venture capital, including private foundations, states, and wealthy individuals (called angel investors), are helping start-up firms find equity capital. These private investors are motivated by the potential to earn a high return on their investment.

What Securities Trade in the Capital Markets?

Stocks, bonds, and other securities trade in securities markets. These markets streamline the purchase and sales activities of investors by allowing transactions to be made quickly and at a fair price. Securities are investment certificates that represent either equity (ownership in the issuing organization) or debt (a loan to the issuer). Corporations and governments raise capital to finance operations and expansion by selling securities to investors, who in turn take on a certain amount of risk with the hope of receiving a profit from their investment.

Securities markets are busy places. On an average day, individual and institutional investors trade billions of shares of stock in more than 10,000 companies through securities markets. Individual investors invest their own money to achieve their personal financial goals. Institutional investors are investment professionals who are paid to manage other people’s money. Most of these professional money managers work for financial institutions, such as banks, mutual funds, insurance companies, and pension funds. Institutional investors control very large sums of money, often buying stock in 10,000-share blocks. They aim to meet the investment goals of their clients. Institutional investors are a major force in the securities markets, accounting for about half of the dollar volume of equities traded.

Types of Markets

Securities markets can be divided into primary and secondary markets. The primary market is where new securities are sold to the public, usually with the help of investment bankers. In the primary market, the issuer of the security gets the proceeds from the transaction. A security is sold in the primary market just once — when the corporation or government first issues it. The Google Blue IPO is an example of a primary market offering.

Later transactions take place in the secondary market, where old (already issued) securities are bought and sold, or traded, among investors. The issuers generally are not involved in these transactions. The vast majority of securities transactions take place in secondary markets, which include broker markets, dealer markets, the over-the-counter market, and the commodities exchanges. You will see tombstones, announcements of both primary and secondary stock and bond offerings, in the Globe and Mail; and other newspapers.

The Role of Investment Bankers and Stockbrokers

Two types of investment specialists play key roles in the functioning of the securities markets. Investment bankers help companies raise long-term financing. These firms act as intermediaries, buying securities from corporations and governments and reselling them to the public. This process, called underwriting, is the main activity of the investment banker, which acquires the security for an agreed-upon price and hopes to be able to resell it at a higher price to make a profit. Investment bankers advise clients on the pricing and structure of new securities offerings, as well as on mergers, acquisitions, and other types of financing. Well-known investment banking firms include Goldman Sachs, Morgan Stanley, and (Canada) BMO Nesbitt Burns, Inc., RBC Capital Markets LLC, and Canaccord Genuity Corp.

A stockbroker is a person who is licensed to buy and sell securities on behalf of clients. Also called account executives, these investment professionals work for brokerage firms and execute the orders customers place for stocks, bonds, mutual funds, and other securities. Investors are wise to seek a broker who understands their investment goals and can help them pursue their objectives.

Brokerage firms are paid commissions for executing clients’ transactions. Although brokers can charge whatever they want, most firms have fixed commission schedules for small transactions. These commissions usually depend on the value of the transaction and the number of shares involved.

Online Investing

Improvements in internet technology have made it possible for investors to research, analyze, and trade securities online. Today almost all brokerage firms offer online trading capabilities. Online brokerages are popular with “do-it-yourself” investors who choose their own stocks and don’t want to pay a full-service broker for these services. Lower transaction costs are a major benefit. Fees at online brokerages range from about $4.95 to $8.00, depending on the number of trades a client makes and the size of a client’s account. Although there are many online brokerage firms, the four largest — Charles Schwab, Fidelity, TD Ameritrade, and E*Trade — account for more than 80 percent of all trading volume and trillions in assets in customer accounts.[10]

In Canada the highest ranking include: Questrade, Interactive Brokers, TD Direct Investing, and CIBC Investor’s Edge. The internet also offers investors access to a wealth of investment information, for example, Qtrade Investor, rated (2021) best for Research.

Investing in Bonds

The terms “bonds” and “fixed income” are often used interchangeably, but in fact, bonds are only one type of fixed income investment in a family (asset class) which includes guaranteed investment certificates (GICs), and money market securities. Typically, these products generate a predictable stream of interest income and/or promise of a future lump sum payment and can be a great way to achieve diversification in your portfolio.

When many people think of financial markets, they picture the equity markets. However, the bond markets are huge. According to Bloomberg News Canada July 16, 2021,[11] Canadian companies are issuing new bonds at a record-breaking pace. In 2021, Canadian companies took advantage of low rates to refinance and fund post-pandemic investments, putting them on-track to exceed the record of $111 billion sold in 2020.

Bonds can be bought and sold in the securities markets. However, the price of a bond changes over its life as market interest rates fluctuate. When the market interest rate drops below the fixed interest rate on a bond, it becomes more valuable, and the price rises. If interest rates rise, the bond’s price will fall. Corporate bonds, as the name implies, are issued by corporations. They usually have a par value of $1,000. They may be secured or unsecured (called debentures), include special provisions for early retirement, or be convertible to common stock. Corporations can also issue mortgage bonds, bonds secured by property such as land, buildings, or equipment.

In addition to regular corporate debt issues, investors can buy high-yield, or junk, bonds — high-risk, high-return bonds often used by companies whose credit characteristics would not otherwise allow them access to the debt markets. They generally earn 3 percent or more above the returns on high-quality corporate bonds. Corporate bonds may also be issued with an option for the bondholder to convert them into common stock. These convertible bonds generally allow the bondholder to exchange each bond for a specified number of shares of common stock. Elon Musk and his electric car company, Tesla, issued high-yield junk bonds in August 2017 and raised nearly $1.8 billion to help finance the production and launch of Tesla’s new Model 3. Tesla has spent billions of dollars in its efforts to develop electric cars in the past few years.[12]

Canadian Government, Provincial and Municipal Bonds and Securities

Federal, provincial and municipal governments issue bonds to fund deficits or to raise capital for program spending. Generally, maturity terms range from over two to 30 years and interest is payable on a semi-annual basis. The most highly-traded bond issues have terms of five, 10, and 30 years. As discussed earlier, corporate bonds are debts issued by companies to raise capital to finance operations and projects. Corporate bonds are riskier than government bonds and have a higher risk of default. However, the increased risk generally comes with higher returns than safer government bonds. Liquidity varies depending on the issuer. See below Summary of Government of Canada (GOC) Bonds, Provincial Bonds and Municipal Bonds from RBC – Understanding Fixed Income.[13]

| Government of Canada (GOC) Bonds | Provincial Bonds | Municipal Bonds | |

|---|---|---|---|

| Rating | AAA rating | Vary in credit rating depending on the province’s power of taxation and the creditworthiness of the debt | Vary in credit rating depending on the municipality’s power of taxation and the creditworthiness of the debt. |

| Yield | Highest credit quality and most conservative bond available in Canada | Have higher yields than GOC bonds | May have higher or lower yields than provincial issues of the same quality, depending on specific issues and liquidity. |

| Guaranteed? | Guaranteed by the federal government | Guaranteed by issuing province | Not automatically guaranteed by the provinces in which they operate |

Strip Coupons and Residual Bonds

Coupons are created from federal, provincial, or municipal bonds whose two basic components — the semi-annual interest payments (coupons) and the principal amount (the residual) — are separated and sold as individual securities. These instruments are purchased at a discount and mature at par (100% or $100). Generally, the longer the term to maturity, the greater the discount. Coupons and residuals pay no interest until maturity and entitle the holder to the security’s full face value at maturity. The interest compounds annually at the yield to maturity at the time of purchase. For example, a Canadian strip coupon maturing in five years with a yield of 6% would be priced at $74.72 and mature at $100. Although no money is paid out until maturity, the interest on the bond accrues each year and must be included as income on income tax records annually. Compared with conventional bonds, strip coupons eliminate reinvestment risk over the term of the investment by paying no cash flows until maturity. Coupons may offer higher yields than bonds but its price will fluctuate more than a bond of similar term and credit quality. Coupons offer investors safety (most are government or high-quality corporate-backed), and an attractive guaranteed yield if held to maturity. Strip coupons remain a popular choice for tax-sheltered accounts such as RRSPs and RRIFs.

Bond Ratings

Bonds vary in quality, depending on the financial strength of the issuer. Because the claims of bondholders come before those of stockholders, bonds are generally considered less risky than stocks. However, some bonds are in fact quite risky. Companies can default — fail to make scheduled interest or principal payments — on their bonds. Investors can use bond ratings, letter grades assigned to bond issues to indicate their quality or level of risk. Ratings for corporate bonds are easy to find. The two largest and best-known rating agencies are Moody’s and Standard & Poor’s (S&P), whose publications are in most libraries and in stock brokerages. Table 17.3 lists the letter grades assigned by Moody’s and S&P. A bond’s rating may change if a company’s (or country’s) financial condition changes.

| Moody’s Ratings | S & P Ratings | Description |

|---|---|---|

| Aaa | AAA | Prime-quality investment bonds: Highest rating assigned; indicates extremely strong capacity to pay. |

| Aa, A | AA, A | High-grade investment bonds: Also considered very safe bonds, although not quite as safe as Aaa/AAA issues; Aa/AA bonds are safer (have less risk of default) than single As. |

| Baa | BBB | Medium-grade investment bonds: Lowest of investment-grade issues; seen as lacking protection against adverse economic conditions. |

| Ba B |

BB B |

Junk bonds: Provide little protection against default; viewed as highly speculative. |

| Caa Ca C |

CCC CC C D |

Poor-quality bonds: Either in default or very close to it. |

Money Market Products

Treasury Bills

Money market products such as treasury bills (T-bills), commercial paper and banker’s acceptances are short-term fixed income products that are sold at a discount and mature at par (face value). The difference between your purchase price and par value is your return. T-Bills are short-term debt instruments issued by federal and provincial governments. Fully backed by the applicable government issuer, a high level of security makes T-Bills a popular investment for individual, institutional, and corporate investors. T-bills are considered very safe because they are fully guaranteed by the issuing government; however, they offer considerably lower potential returns than most other securities. The difference between your purchase price and par value is your return and it is considered interest income.

Banker’s Acceptances (BAs)

BAs are short-term credit investments created by a borrower for payment on a specified future date. BAs are “accepted” or guaranteed at maturity by banks and offer a high degree of safety for short-term investors.

Commercial Paper (CP)

CP investments are unsecured promissory notes issued by corporations. Companies issue CP to finance seasonal cash flow and working capital needs at lower rates than conventional bank loans.

Crown Corporate Paper

Crown corporations are state-owned enterprises owned by the Sovereign of Canada. Short-term promissory notes are issued by crown corporations such as the Canadian Mortgage and Housing Corporation, Federal Business Development Bank, Export Development Corporation or Canadian Wheat Board. Many crown corporations issue commercial paper denominated in both Canadian and U.S. dollars.

Other Popular Securities

In addition to stocks and bonds, investors can buy Guaranteed Investment Certificates (GICs), mutual funds, or exchange-traded funds (ETFs). Futures contracts and options are more complex investments for experienced investors.

Guaranteed Investment Certificates

A Guaranteed Investment Certificate (GIC) is a deposit investment issued by financial institutions such as chartered banks, trust companies and mortgage and loan companies. GICs offer a specified rate of return for a set period.

Many GICs are guaranteed by the Canada Deposit Insurance Corporation (CDIC) for up to $100,000 (this includes both principal and interest), provided that certain criteria are met. Each individual issuer can provide full CDIC coverage, which means that you could invest, for example, $400,000 with four different issuers — all completely CDIC insured and in one account. In addition, the CDIC coverage applies to each registration. For example, with one issuer you could have $100,000 in each of a GIC, an RRSP, a RRIF and a TFSA and they would all be covered.

Mutual Funds

Suppose that you have $1,000 to invest but don’t know which stocks or bonds to buy, when to buy them, or when to sell them. By investing in a mutual fund, you can buy shares in a large, professionally managed portfolio, or group, of stocks and bonds. A mutual fund is a financial service company that pools its investors’ funds to buy a selection of securities — marketable securities, stocks, bonds, or a combination of securities — that meet its stated investment goals. Each mutual fund focuses on one of a wide variety of possible investment goals, such as growth or income. Many large financial service companies, such as BMO Investments Inc., CIBC Securities Inc., and Manulife Securities Investments Services Inc., sell a wide variety of mutual funds, each with a different investment goal. Investors can pick and choose funds that match their particular interests. Some specialized funds invest in a particular type of company or asset: in one industry such as health care or technology, in a geographical region such as Asia, or in an asset such as precious metals.

Mutual funds are one of the most popular investments for individuals today; they can choose from about 9,500 different funds. Investments in mutual funds amount to more than $40 trillion worldwide, of which U.S. mutual funds hold more than $19 trillion. Mutual funds appeal to investors for three main reasons:

- They are a good way to hold a diversified, and thus less risky, portfolio. Investors with only $500 or $1,000 to invest cannot diversify much on their own. Buying shares in a mutual fund lets them own part of a portfolio that may contain 100 or more securities.

- Mutual funds are professionally managed.

- Mutual funds may offer higher returns than individual investors could achieve on their own.

Exchange-Traded Funds

Another type of investment, the exchange-traded fund (ETF), has become very popular with investors. ETFs are similar to mutual funds because they hold a broad basket of stocks with a common theme, giving investors instant diversification. ETFs trade on stock exchanges (most trade on the American Stock Exchange, AMEX), so their prices change throughout the day, whereas mutual fund share prices, called net asset values (NAVs), are calculated once a day, at the end of trading. Investors can choose from more than 1,700 ETFs that track almost any market sector and industry sectors such as health care or energy, and geographical areas such as a particular country (Japan) or region (Latin America). In Canada there are over 700 ETFs listed on the TSX (Toronto Stock Exchange). ETFs have very low expense ratios. However, because they trade as stocks, investors pay commissions to buy and sell these shares.

Futures Contracts and Options

Futures contracts are legally binding obligations to buy or sell specified quantities of commodities (agricultural or mining products) or financial instruments (securities or currencies) at an agreed-on price at a future date. An investor can buy commodity futures contracts in cattle, pork bellies (large slabs of uncured bacon), eggs, coffee, flour, gasoline, fuel oil, lumber, wheat, gold, and silver. Financial futures include Treasury securities and foreign currencies, such as the British pound or Japanese yen. Futures contracts do not pay interest or dividends. The return depends solely on favorable price changes. These are very risky investments because the prices can vary a great deal and are considered speculative for retail investors.

Options are contracts that entitle holders to buy or sell specified quantities of common stocks or other financial instruments at a set price during a specified time. As with futures contracts, investors must correctly guess future price movements in the underlying financial instrument to earn a positive return. Unlike futures contracts, options do not legally obligate the holder to buy or sell, and the price paid for an option is the maximum amount that can be lost. However, options have very short maturities, so it is easy to quickly lose a lot of money with them.

Where can Investors Buy and Sell Securities, and How are Securities Markets Regulated?

When we think of stock markets, we are typically referring to secondary markets, which handle most of the securities trading activity. The two segments of the secondary markets are broker markets and dealer markets. The primary difference between broker and dealer markets is the way each executes securities trades. Securities trades can also take place in alternative market systems and on non-U.S. securities exchanges.

The securities markets both in Canada and around the world are in flux and undergoing tremendous changes. We present the basics of securities exchanges in this section and discuss the latest trends in the global securities markets later in the chapter.

Broker Markets

The broker market consists of national and regional securities exchanges that bring buyers and sellers together through brokers on a centralized trading floor. In the broker market, the buyer purchases the securities directly from the seller through the broker. Broker markets account for about 60 percent of the total dollar volume of all shares traded in the U.S. securities markets.

Canadian Stock Exchange

TMX Group is an integrated, multi-asset class exchange group. TMX Group’s key subsidiaries operate cash and derivative markets and clearinghouses for multiple asset classes including equities, fixed income and energy. The TMX owns and operates Toronto Stock Exchange (TSX) which is Canada’s senior equities market, providing issuers with a venue for raising capital and providing domestic and international investors with the opportunity to invest in and trade those issuers’ securities.

- TMX also owns the TSX Venture Exchange. TSX Venture Exchange is Canada’s premier junior listings market, providing companies at the early stages of growth with the opportunity to raise capital and providing investors with the opportunity to invest in and trade those issuers’ securities.

- TSX Trust: TSX Trust is a provider of corporate trust, securities transfer and registrar, and employee plan administration services for issuers.

- Montréal Exchange: Montréal Exchange is Canada’s standardized financial derivatives exchange. Headquartered in Montréal, MX offers trading in interest rate, index and equity derivatives.

- TSX Alpha Exchange: TSX Alpha Exchange is an exchange that provides equities trading for TSX and TSXV listed securities.

- Shorcan: Shorcan is Canada’s first inter-dealer broker (IDB), providing facilities for matching orders for Canadian federal, provincial, corporate and mortgage bonds and treasury bills and derivatives for anonymous or name-give-up buyers and sellers in the secondary market.

- Canadian Derivatives Clearing Corporation(CDCC) offers clearing and settlement services for all MX transactions and certain over-the-counter (OTC) derivatives, including fixed income repurchase and reverse repurchase agreement (REPO) transactions.

- Canadian Depository for Securities(CDS) is Canada’s national securities depository, clearing and settlement hub. CDS supports Canada’s equity, fixed income and money markets and is accountable for the safe custody and movement of securities, the processing of post-trade transactions, and the collection and distribution of entitlements relating to securities deposited by participants.

- TMX Insights delivers financial content, tools and applications, as well as analytics to drive better markets and investment decisions.

- Trayport is a leading provider of energy trading solutions to traders, brokers and exchanges worldwide.

- TMX Money provides investors with powerful investment tools and resources. It is the trusted Canadian source for current market data, index, and company information for the Canadian and US markets.

Dealer Markets

Unlike broker markets, do not operate on centralized trading floors but instead use sophisticated telecommunications networks that link dealers throughout Canada. Buyers and sellers do not trade securities directly, as they do in broker markets. They work through securities dealers called market makers, who make markets in one or more securities and offer to buy or sell securities at stated prices. A security transaction in the dealer market has two parts: the selling investor sells his or her securities to one dealer, and the buyer purchases the securities from another dealer (or in some cases, the same dealer).

The Over-the-Counter Market

The over-the-counter (OTC) markets refer to those other than the organized exchanges. There are two OTC markets: the Over-the-Counter Bulletin Board (OTCBB) and the Pink Sheets. These markets generally list small companies and have no listing or maintenance standards, making them attractive to young companies looking for funding. OTC market has no trading floor. It consists of many people in different locations who hold an inventory of securities that are not listed on any of the major exchanges. The OTC market consists of independent dealers who own the securities that they buy and sell at their own risk. Investing in OTC companies is highly risky and should be for experienced investors only.

NASDAQ

The largest dealer market is the National Association of Securities Dealers Automated Quotation system, commonly referred to as NASDAQ. The first electronic-based stock market, the NASDAQ is a sophisticated telecommunications network that links dealers throughout the world. Its sophisticated electronic communication system provides faster transaction speeds than traditional floor markets and is the main reason for the popularity and growth of the OTC market. The NASDAQ lists more companies than the NYSE, but the NYSE still leads in total market capitalization. Many newer firms are listed there when their stocks first become available in the secondary market. Highly traded listings include Apple, Microsoft, Intel, and Netflix.

Watch How to read a stock quote from RBC.

Alternative Trading Systems

In addition to broker and dealer markets, alternative trading systems such as electronic communications networks (ECNs) make securities transactions. ECNs are private trading networks that allow institutional traders and some individuals to make direct transactions in what is called the fourth market. ECNs bypass brokers and dealers to automatically match electronic buy and sell orders. They are most effective for high-volume, actively traded stocks. Money managers and institutions such as pension funds and mutual funds with large amounts of money to invest like ECNs because they cost far less than other trading venues.

Global Trading and Foreign Exchanges

Improved communications and the elimination of many legal barriers are helping the securities markets go global. The number of securities listed on exchanges in more than one country is growing. Foreign securities are now traded in the United States. Likewise, foreign investors can easily buy U.S. securities.

Stock markets also exist in foreign countries; more than 60 countries operate their own securities exchanges. NASDAQ ranks second to the NYSE, followed by the London Stock Exchange (LSE) and the Tokyo Stock Exchange. Other important foreign stock exchanges include Euronext (which merged with the NYSE but operates separately) and those in Toronto, Frankfurt, Hong Kong, Zurich, Australia, Paris, India and Taiwan. Why should U.S. investors pay attention to international stock markets? Because the world’s economies are increasingly interdependent, businesses must look beyond their own national borders to find materials to make their goods and markets for foreign goods and services. The same is true for investors, who may find that they can earn higher returns in international markets.

Regulation of Securities Markets

In Canada, the regulation of securities markets is a provincial responsibility. Canada has a number of provincial securities commissions, such as the British Columbia Securities Commission, the Québec Securities Commission (Québec Autorité des marchés financiers), and the New Brunswick Financial and Consumer Services Commission. These commissions oversee the securities industry and the capital markets across Canada and administer and enforce provincial securities legislation, such as the Securities Act.

Regulators protect investors by making and enforcing rules for the securities industry in Canada. In Canada, we have two main bodies protecting investors: Provincial and Territorial Securities Regulators and Industry Self-Regulatory Organizations and Groups (SROs).

1. Provincial and Territorial Securities Commissions

Provincial securities commissions are mandated to protect investors from unfair, improper, or fraudulent practices and to foster fair and efficient capital markets. They do this by:

- registering and supervising those in the business of advising on or trading in securities;

- supporting self-regulation of the securities markets and overseeing the self-regulatory organizations;

- ensuring that investors have access to the information they need to make informed investment decisions; and

- conducting investigations and bringing enforcement actions for serious infractions of securities law.

In Canada, provincial and territorial securities commissions, such as the BC Securities Commission or Ontario Securities Commission (OSC), administer and enforce rules around how securities are issued, bought and sold, and set minimum entry standards for market intermediaries who deal with investors. Anyone who sells securities or gives advice about securities must be registered with their provincial commission. Different types of registration can be held by an investment representative or the sponsoring firm. Individuals or firms that are registered are called “registrants.” The type of registration determines what kinds of investment products the registrants are licensed to sell or the types of services they can provide.

Securities regulators also regulate marketplaces and clearing agencies, oversee the Investment Industry Regulatory Organization of Canada (IIROC) and the Mutual Fund Dealers Association of Canada (MFDA), approve individuals and firms for regulation based on proficiency and educational requirements, and discipline firms and individuals. Securities regulators work together through the Canadian Securities Administrators (CSA).

2. Self-Regulatory Organizations (SROs)

The investment community also regulates itself, developing and enforcing ethical standards to reduce the potential for abuses in the financial marketplace. In Canada, SROs regulate their members’ standards of practice and business conduct in order to promote investor protection. Canada has two main SROs:

- IIROC sets and enforces rules for investment dealers and for equity marketplaces like the Toronto Stock Exchange and TSX Venture Exchange. It also monitors trading on those marketplaces, approves training courses and disciplines member firms and individuals.

- The MFDA sets and enforces rules for mutual fund dealers and disciplines member firms and individuals.

In Quebec, the Montréal Exchange is also considered an SRO. MX is the only financial derivatives exchange in Canada, and currently lists equity options, options on ETFs, currency options, index derivatives, and interest rate derivatives.

Securities Legislation

Canada does not have comprehensive federal securities legislation or federal regulatory body. Government regulation is primarily provincial and emphasizes self-regulation though the various provincial securities exchanges.

The meaning of insider was expanded beyond a company’s directors, employees, and their relatives to include anyone who gets private information about a company. The B.C. Securities Act, Securities Regulation, and Securities Rules, as well as national, multi-lateral, and B.C. instruments regulate trading in securities and derivatives in the province of British Columbia.

Risk Management

Canadian financial institutions face an increasingly complex regulatory web as regulators in Canada and globally are imposing greater pressures to assess, monitor and mitigate regulatory and operational risks. Also, today’s financial institutions need to keep up with new regulations, deal with new issues, including those created by remote work and emerging technologies, and manage the human resources and technological requirements to get the job done. The speed of change is rapid and the demands are increasing.

Risk is defined as the uncertainty about future events; various risks originate due to the uncertainty arising out of various factors that influence an investment or a situation. Businesses face two basic types of risk: speculative risks, such as financial investments, including the possibility of a gain or loss, and pure risk, which includes all the possibility of loss or no loss. Managing these risks is important for companies to survive and prosper.

Risk management in the financial world is the process of identification, analysis, and acceptance or mitigation of uncertainty in investment decisions. Essentially, risk management occurs when an investor or fund manager analyzes and attempts to quantify the potential for losses in an investment. There are five steps to Risk Management:

- Identify Risks and Potential Losses.

- Measure the Frequency and Impact.

- Evaluate Alternatives and Respond; respond options include:

- Avoidance — refuse to participate in ventures that carry any risk:

- Control — techniques to prevent, minimize, or reduce losses or consequences of losses;

- Retention — covering unavoidable losses with its own funds; and

- Transfer — transfer of risk to another individual or firm by contract.

- Implement Choice of Risk Response.

- Monitor Results.

Comprehensive Check

- What is the main goal of the financial manager? How does the risk-return trade-off relate to the financial manager’s main goal?

- Distinguish between short- and long-term expenses.

- Describe a firm’s main motives in making capital expenditures.

- Why might firms choose factoring instead of loans?

- Distinguish between unsecured and secured short-term loans.

- Briefly describe the three main types of unsecured short-term loans.

- Distinguish between debt and equity.

- Briefly describe these sources of equity: retained earnings, preferred stock, and venture capital.

- Why do mutual funds and exchange-traded funds appeal to investors?

Key Takeaways

- The key activities of the financial manager are:

- financial planning;

- investment; and

- financing.

- Financial management — the art and science of managing a firm’s money so that it can meet its goals — is not just the responsibility of the finance department. All business decisions have financial consequences. Managers in all departments must work closely with financial personnel.

- Risk-return trade-off is a concept in finance that explains the principle that the higher the risk, the greater the return that is required.

- Short-term expenses support the firm’s day-to-day activities, and long-term expenses are typically for fixed assets.

- Financial managers must choose the best mix of debt and equity for their firm. The main advantage of debt financing is the tax-deductibility of interest. But debt involves financial risk because it requires the payment of interest and principal on specified dates. Equity — common and preferred stock — is considered a permanent form of financing on which the firm may or may not pay dividends. Dividends are not tax-deductible.

- The main types of long-term debt are term loans, bonds, and mortgage loans.

- The main sources of equity financing are common stock, retained earnings, and preferred stock.

- Securities markets allow stocks, bonds, and other securities to be bought and sold quickly and at a fair price. New issues are sold in the primary market. After that, securities are traded in the secondary market. Investment bankers specialize in issuing and selling new security issues. Stockbrokers are licensed professionals who buy and sell securities on behalf of their clients.

- Competition among the world’s major securities exchanges has changed the composition of the financial marketplace.

Attributions

This Chapter is adapted from Introduction to Business – licensed under a Creative Commons Attribution 4.0 International CC BY-NC-SA (Attribution NonCommercial ShareAlike) license, which means that you can distribute, remix, and build upon the content, as long as you provide attribution to OpenStax and its content contributors. The chapter differ from the original to reflect Canadian content.

The original OpenStax content can be found here: section 16.5 Equity Financing in Introduction to Business.

- What challenges do today’s financial managers face? CFO magazine at http://www.cfo.com ↵

- Royal Bank of Canada. (n.d.). Cash Management & Payment Solutions. http://www.rbcroyalbank.com/caribbean/bb/business/cash-management-payment-solutions/home.html ↵

- Kelly, S. (2017, March 20). Credit Management Technology Plays Catch-Up. Treasury & Risk. https://www.treasuryandrisk.com/2017/03/20/credit-management-technology-plays-catch-up/?slreturn=20230024165817 ↵

- Bramwell, J. (2013, December 16). CFOs More Likely to Outsource Accounting and Finance Projects. Accounting Web. Retrieved October 10, 2017, from https://www.accountingweb.com/practice/team/cfos-more-likely-to-outsource-accounting-and-finance-projects ↵

- McKay, P. (2017, October 6). Why Going Public Doesn’t Make Sense Right Now. Fortune. https://fortune.com/2017/09/13/going-public-snap-blue-apron-ipo-stock-price/ ↵

- Kochkodin, B. (2017, August 10). Blue Apron is the IPO Bust of the Decade. Bloomberg. https://www.bloomberg.com/news/articles/2017-08-10/blue-apron-down-44-is-the-ipo-bust-of-the-decade-chart ↵

- Snider, M. (2018, April 4). Spotify goes public: What you need to know about the music streamer and its IPO. USA TODAY. https://eu.usatoday.com/story/tech/talkingtech/2018/04/03/spotify-goes-public-what-you-need-know-music-streamer-and-its-ipo/480318002/ ↵

- CIBC Investor Relations. (n.d.). CIBC Common Dividends. https://www.cibc.com/en/about-cibc/investor-relations/share-information/common-share-information/common-dividends.html ↵

- Vascellaro, J. E. (2012, March 21). Apple to Pay Dividend, Plans $10 Billion Buyback. WSJ. Retrieved October 10, 2017, from https://www.wsj.com/articles/SB10001424052702304724404577291071289857802 ↵

- Woolley, S. (2017, February 27). TD Ameritrade Jumps into Price War with Fidelity and Schwab. Bloomberg. https://www.bloomberg.com/news/articles/2017-02-28/fidelity-slashes-commissions-in-the-latest-salvo-in-the-fee-wars#xj4y7vzkg ↵

- Duarte, E. (2021, July 16). Canadian companies are issuing new bonds at a record pace. BNN Bloomberg. https://www.bnnbloomberg.ca/canadian-companies-are-issuing-new-bonds-at-a-record-pace-1.1629944 ↵

- Sifma. (2016). 2016 Year in Review. Retrieved October 10, 2017, from https://www.sifma.org/wp-content/uploads/2017/05/2016-year-in-review.pdf ↵

- Royal Bank of Canada. (n.d.). Types of Fixed Income. https://www6.royalbank.com/en/di/reference/article/fixed-income-types/j7cypocm ↵

Key terms appear throughout the chapter. When you click on them, a definition will pop up. If you are using a downloaded or printed format, check the glossary in the back of the book. Please make sure you can define them!

Financial Management is the art and science of managing a firm’s money so that it can meet its goals.

Risk-return trade off Is a concept which explains the basic principle in finance that the higher the risk, the greater the return that is required.

Current assets, include cash and any other assets (accounts receivable and inventory) that can be converted to cash within a year.

The process of making sure that a firm has enough cash on hand to pay bills as they come due and to meet unexpected expenses.

The inflow and outflow of cash for a business.

Market securities are short-term investments that are easily converted into cash.

Commercial paper is unsecured short-term debt—an IOU—issued by a financially strong corporation.

Sales for which a firm has not yet been paid.

Investments in long-lived assets, such as land, buildings, machinery, equipment, and information services, that are expected to provide benefits over a period longer than one year.

The process of analyzing long-term projects and selecting those that offer the best returns while maximizing the firm’s value.

Loans for which the borrower does not have to pledge specific assets as security.

The extension of credit by the seller to the buyer between the time the buyer receives the goods or services and when it pays for them.

Purchases for which a buyer has not yet paid the seller.

Factoring is a form of short-term financing in which a firm sells its accounts receivable outright at a discount to a factor.

Financial risk is the chance that the firm will be unable to make scheduled interest and principal payments.

Term loan is a business loan with a maturity of more than one year. Term loans generally have maturities of 5 to 12 years and can be unsecured or secured.

Bonds are long-term debt obligations (liabilities) of corporations and governments. A bond certificate is issued as proof of the obligation.

Principal is the amount borrowed.

Mortgage loan is a long-term loan made against real estate as collateral.

Payments to stockholders from a corporation’s profits.

Payments to stockholders in the form of more stock; may replace or supplement cash dividends.

Profits that have been reinvested in a firm.

An equity security for which the dividend amount is set at the time the stock is issued and the dividend must be paid before the company can pay dividends to common stockholders.

Investment professionals who are paid to manage other people’s money.

The securities market where new securities are sold to the public.

The securities market where old (already issued) securities are bought and sold, or traded, among investors; includes broker markets, dealer markets, the over-the-counter market, and the commodities exchanges.

Firms that act as intermediaries, buying securities from corporations and governments and reselling them to the public.

The process of buying securities from corporations and governments and reselling them to the public; the main activity of investment bankers.

A person who is licensed to buy and sell securities on behalf of clients.

Letter grades assigned to bond issues to indicate their quality or level of risk; assigned by rating agencies such as Moody’s and Standard & Poor’s (S&P).

A financial-service company that pools investors’ funds to buy a selection of securities that meet its stated investment goals.

Risk is the uncertainty about future events. It is the potential for loss or the chance that an investment will not achieve the expected level of return.