2.4 Understanding Budgets

Budgeting is an exercise in refining the focus of the project. As explain earlier progressive elaboration enables us to start with a wide-angle estimate, in which the details are necessarily fuzzy, and bit by bit zero in on a sharper picture of project costs. In some projects there is the attempt to nail down every figure in an early draft of a budget but in fact only develop a budget at the precision needed for current decisions since overall precision can and should advance as the project advances.

In the early stages of the budgeting process a percentage for uncertainty must be included. The percentage may initially be large but should gradually decrease as the project progresses and the level of uncertainty declines. For IT projects, which are notoriously difficult to estimate, adding an uncertainty percentage to every line item is good practice. Some items, such as hardware, might be easy to estimate. But other items, such as labor to create innovative technology, can be extremely difficult to estimate. These line item variances can influence the total estimate variance by a significant amount in many projects. Including a contingency fund, which is a percentage of the budget must be set aside for unforeseen costs.

Successful project managers use the budgeting process as a way to create stakeholder buy-in regarding the use of available resources to achieve the intended outcome. By being as transparent as possible about costs and resource availability helps with building trust among stakeholders. By taking care to use the right kinds of contracts—for example, contracts that do not penalize stakeholders for escalating prices caused by a changing economy—may can create incentives that keep all stakeholders focused on delivering the project value, rather than merely trying to protect their own interests.

Cost Budgeting

The main goal of the cost budgeting process is to produce a cost baseline. This baseline is a time-phased budget that can be used to measure and monitor cost performance after it has been approved by the key project stakeholders. The aggregated budget is integrated with the project schedule to produce the time-phased budget. Costs are associated with tasks, and since each task has a start date and a duration period, it is possible to calculate how much money will be spent by any date during the project. Recognizing that all the money required to deliver the project is not needed upfront, allows the cash flow needs of the project to be effectively managed.

For smaller organizations facing cash flow challenges, this can result in significant savings as the money required to pay for resources can be transferred to the project account shortly before it is needed. These transfers must be timed so that the money is there to pay for each task without causing a delay in the start of the task. If the money is transferred too far in advance, the organization will lose the opportunity to use the money somewhere else, or they will have to pay unnecessary interest charges if the money is borrowed.

Managing Cash Flow

If the total amount spent on a project is equal to or less than the amount budgeted, the project can still be in trouble if the funding for the project is not available when it is needed. There is a natural tension between the financial people in an organization, who do not want to pay for the use of money that is just sitting in a checking account, and the project manager, who wants to be sure that there is enough money available to pay for project expenses. The financial people prefer to keep the company’s money working in other investments until the last moment before transferring it to the project account. The contractors and vendors have similar concerns, and they want to get paid as soon as possible so they can put the money to work in their own organizations. The project manager would like to have as much cash available as possible to use if activities exceed budget expectations.

Managing the Budget

A key aspect of ongoing cost management is monitoring cost estimates. Baseline budgets often change after they have been approved. Successful project leaders understand that estimates are just that, estimates. As new information and real experience occur, it may be necessary to revise an estimate. In some cases, the revision is minor and does not impact the achievement of the project’s total budget. In other instances, the necessary revisions are significant, and a new baseline needs to be created.

It is important for project managers to discuss the ongoing management of the schedule with key stakeholders to understand their expectations of when/how they are informed of changes that need to be made. Large complex projects may document stakeholders’ expectations for ongoing cost management in a formal Cost Management Plan. In addition, there are several tools and techniques that help project leaders monitor and control project budgets.

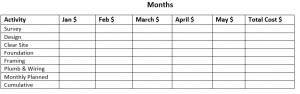

Example of Budget 1

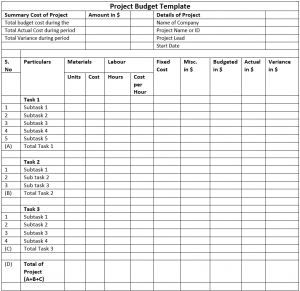

Example of Budget 2

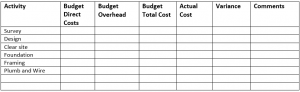

Example of Budget 3