4.4 Contract Types

There are three primary types of contracts – fixed price, cost reimbursable, and time and materials. The objective is to select the type that creates the fairest and most workable deal for both parties – the project team (client) and the contractor (vendor).

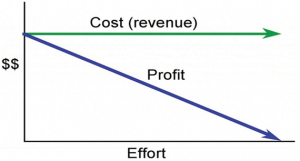

Fixed-Price Contracts

In a fixed price contract, no matter how much time or effort goes into the project, the project always pays the same. As displayed in Exhibit 4.2, the cost to the client remains unchanged while the profit to the vendor decreases as more effort is exerted.

The fixed-price contract is a legal agreement between a client (the organization leading the project) and a vendor (person or company) that will provide goods or services for the project at an agreed-on price. The vendor is responsible for incorporating all costs, including profit, into the agreed-on price. The vendor also assumes the risks for unexpected increases in labour and materials needed to provide the service or materials and in the materials and timeliness required.

The contract usually details the quality of the goods or services, timing needed to support the project, and price for delivering goods or services. There are several variations of the fixed-price contract. The fixed-price contract offers a predictable cost for commodities, goods, and services where the scope of work is evident and unlikely to change. The responsibility for managing the work to meet the needs of the project is focused on the vendor. The project team tracks the quality and schedule progress to ensure the vendor(s) will meet the project needs. Contracts carry a degree of risk. For fixed-price contracts, the risks are the costs associated with project change. If a change occurs on the project that requires a change order from the vendor, the price of the change is typically very high.

Fixed-price contracts require the availability of vendors with appropriate qualifications and performance histories to ensure that the project’s needs can be met. The other requirement is a scope of work that is most likely not going to change—developing a clear scope of work based on good information, creating a list of highly qualified bidders, and developing a clear contract that reflects that scope of work is critical aspects of a good fixed-priced contract. As a result, solutions developed in an iterative fashion (like agile) are generally more challenging to manage with fixed-price contracts.

The fixed-price contract with price adjustment is used for unusually long projects that span years. The main difference is that it considers inflation-adjusted prices. In some countries, the value of its local currency can vary significantly in a few months, which affects the cost of local materials and labour. In periods of high inflation, the contract price is adjusted accordingly. If the adjustment is determined upfront and included in the fixed price, the project accepts the risk that the actual inflation rate is lower than stipulated in the contract, and the vendor runs the risk that the actual inflation is higher than stipulated. The volatility of certain commodities can also be accounted for in a price adjustment contract. For example, if the price of oil significantly affects the project’s costs, the contract can allow for an adjustment based on a change in the price of oil.

The fixed-price contract with incentive fee provides an incentive for performing better than stipulated in the contract. A common example is delivering ahead of schedule.

If the service or materials can be measured in standard units, but the amount needed is not known accurately, the price per unit can be fixed—a fixed-unit-price contract. The project team assumes the responsibility of estimating the number of units used. If the estimate is inaccurate, the contract does not need to be changed, but the project will exceed the budgeted cost.

| Type | Known Scope | Share of Risk | Incentive for Meeting Milestones | Predictability of Cost |

| Fixed total cost | Very High | All vendor | Low | Very high |

| Fixed unit price | High | Mostly project | Low | Medium |

| Fixed price with incentive fee | High | All vendor | High | Medium-high |

| Fixed fee with price adjustment | High | Depends on how the adjustment will occur (before or after the trigger for adjustment arises) | Low | Medium |

Cost-Reimbursable Contracts

Cost reimbursable contracts are also called cost-plus contracts. This is where the vendor charges you for the cost of doing the work plus some negotiated fee or rate. Exhibit 4.4 illustrates this by showing that as efforts increase, costs to the client also increase while the vendor’s profits stay the same.

In a cost-reimbursable contract, also known as cost-plus contracts, the organization agrees to pay the vendor for the cost of performing the service or providing the goods. Cost-reimbursable contracts are most often used when the scope of work or the costs for performing the work are not well known. The project uses a cost-reimbursable contract to pay the contractor for allowable expenses related to performing the work. Since the cost of the project is reimbursable, the vendor has much less risk associated with cost increases. When the costs of the work are not well known, a cost-reimbursable contract reduces the amount of contingency the bidders place in their bid to account for the risk associated with potential increases in costs. This type of contract is often well-suited to projects using the agile development methodology.

This is quite different from fixed-price contracts, where vendors try to include as much contingency as possible in their bids to protect their profit margin. In these types of contracts, the vendor is less motivated to find ways to reduce the cost of the project as there is no incentive to do so – the client will reimburse costs incurred by the vendor, even if they are unnecessarily high, as the work is completed. One way to limit excessive costs imposed by vendors is to include incentives for supporting the accomplishment of project goals.

Cost-reimbursable contracts require good documentation of the costs that occurred on the project to ensure that the vendor receives payment for all the work performed and that the organization is not paying for something that was not completed. The vendor is also guaranteed a profit over and above cost reimbursement. There are several ways to compensate the vendor:

- A cost-reimbursable contract with a fixed fee provides the vendor with a profit amount, often referred to as a fee, determined at the beginning of the contract and does not change.

- A cost-reimbursable contract with a percentage fee provides the vendor with a percentage of the allowable costs as profit. For instance, the fee could be 5% of total allowable costs. The vendor is reimbursed for allowable costs and is compensated with a fee that changes as the costs change.

- A cost-reimbursable contract with an incentive fee is used to encourage performance in areas critical to the project. Often the contract attempts to motivate vendors to save or reduce project costs. For instance, besides being reimbursed for allowable costs, the vendor (a talent scout) receives a predetermined bonus fee for each musician who signs on with the record label at a very attractive price.

- A cost-reimbursable contract with award fee reimburses the vendor for all allowable costs plus a fee based on performance criteria. The fee is typically based on goals or objectives that are more subjective. An amount of money is set aside for the vendor to earn through excellent performance, and the decision on how much to pay the vendor is left to the judgment of the project team. The amount is sufficient to motivate excellent performance. For instance, besides being reimbursed for allowable costs, a music producer receives an award fee from the record label based on the album’s rating.

| Cost Reimbursable (CR) | Known Scope | Share of Risk | Incentive for Meeting Milestones | Predictability of Cost |

| CR with fixed fee | Medium | Mostly project | Low | Medium-high |

| CR with percentage fee | Medium | Mostly project | Low | Medium-high |

| CR with incentive fee | Medium | Mostly project | High | Medium |

| CR with award fee | Medium | Mostly project | High | Medium |

| Time and Materials | Low | All project | Low | Low |

Time and Material Contracts

In a time and materials contract, the client pays a rate for the time spent working on the project and pays for all the materials used to do the work. Exhibit 4.5 demonstrates that as costs to the client increase, so does the profit for the vendor.

For project activities with a high level of uncertainty, the vendor might charge an hourly rate for labour, the cost of materials, plus a percentage of the total costs. This type of contract is called time and materials (T&M). Time is usually contracted on an hourly rate, and the vendor would often be required to submit timesheets and receipts for items purchased for the project. The project reimburses the vendor for the time spent at the agreed-on rate and the actual cost of the materials. The fee, which becomes the vendor’s profit margin, is typically a percentage of the total cost.

T&M contracts are used on projects for work that is smaller in scope and has uncertainty or risk. This is often well suited to projects following the agile development methodology. The project, rather than the vendor, assumes all the risk. However, this can be particularly challenging if there are no limits to the amount of effort and materials that can be applied.

To minimize the risk to the project, the vendor typically includes a not-to-exceed amount, which means the contract can only charge up to the agreed amount. The T&M contract allows the project to adjust the contract as more information about the project’s end solution becomes available. The final cost of the work is not known until sufficient information is available to complete a more accurate estimate.

Since there are numerous contract-type alternatives, deciding which type is appropriate for any given project can be challenging. The following considerations can help project teams identify the best alternative for the project:

- Is the required work or materials a commodity, customized product or service, or unique skill or relationship?

- How well-known is the scope of work?

- What are the risks, and which party should assume which types of risk?

- Does the procurement of the service or goods affect activities on the project schedule’s critical path, and how much float is there on those activities?

- How important is it to be sure of the cost in advance?