5.6 Back to Back Annuities

Learning Outcomes

Calculate the initial deposit value or payment sizes in back-to-back annuities.

What are back-to-back annuities? They are a series of equal-sized, regular deposits (payments) over a fixed period of time (annuity 1) followed by a series of equal-size regular withdrawals for a fixed time period (annuity 2). In both cases, the balance in the account will be earning interest during the deposits and withdrawals. See the diagram below:

Notice that, unless there is a special deposit or withdrawal between the two annuities, the ending balance of the first annuity (FV1) becomes the starting value of annuity 2 (PV2) with one caution: we need to be careful of signs. FV1 will be negative. PV2 will be positive (they should be opposite in sign). We will talk more about this later during our first example.

See the sections below for key formulas, tips and examples related to back-to-back annuities calculations.

Examples of back-to-back annuities

It is common when saving for retirement, or for a child’s education to save up by making regular deposits into an RRSP (registered retirement savings plan) or an RESP (registered education savings plan). Often, after making these regular deposits, the retiree (or student) starts making regular withdrawals from the account upon retirement (or upon starting school for the student).

The Signs of PV, PMT & FV for Back-to-Back Annuities

When calculating deposit or withdrawal amounts for back-to-back annuities, it is important to be careful of the signs of each of the values (for PV, PMT and FV). Let’s examine the signs below:

Annuity 1: The initial balance (PV1) is considered positive. This balance gathers interest. The subsequent payments (PMT1) add to the existing balance in the account and are therefore also positive. At the end of the annuity, we consider the future value (FV1) as the amount we would need to withdraw from the account to close the account. For this reason, the future value (FV1) is recorded as negative:

| PV1 | Interest1 | PMT1 | FV1 |

|---|---|---|---|

| Initial Deposit | + % Gain | + Regular Deposits | = Ending Balance |

| 0 or + | + | + | − |

Annuity 2: The initial balance (PV2), in most cases, is the amount of money saved up in annuity 1 (FV1). There is one exception to this rule – when there is a lump-sum deposited or withdrawn between the end of Annuity1 and the start of Annuity2. We will see examples of this later in this section.

| PV2 | Interest2 | PMT2 | FV2 |

|---|---|---|---|

| Initial Deposit | + % Gain | = Regular Withdrawals | + Final Withdrawal |

| + | + | − | 0 or − |

For annuity 2, both the regular withdrawals (PMT2) and the final ending balance (FV2) deduct from the balance in the account. They should both be negative:

Putting this all together gives:

| PV1 | Interest1 | PMT1 | FV1 | PV2 | Interest2 | PMT2 | FV2 |

|---|---|---|---|---|---|---|---|

| Initial Deposit | + % Earned | + Regular Deposits | =Ending Balance Part 1 | =Starting Balance Part 2 | + % Earned | = Regular Withdrawals | + Final Withdrawal |

| + | + | + | − | + | + | − | − |

Notice that, we use the ending balance of annuity 1 (FV1) becomes the starting balance of annuity 2 (PV2) except we change the sign. FV1 should be negative and PV2 should be positive (they should be opposite in sign). We will talk more about this later during our first example.

Determining the size of the Regular deposits (PMT1)

Some people plan for their retirement by deciding on the size of the withdrawals they would like to receive upon retirement (PMT2). They then back-calculate the size of the deposits (PMT1) they will need to make to achieve their retirement goals.

Let's have a look at Raj's retirement plan in the next example. Raj is very wise and starts saving when he turns 25!

Example 5.6.1

Today is Raj’s 25th birthday, and he has opened an account to start his retirement savings with an initial deposit of $1,000. He plans to make regular deposits into the account on a monthly basis, with the first deposit today. He estimated that, the retirement account will earn an average interest rate of 6% compounded annually. At age 65 he will turn his retirement saving into an annuity paying 4% compounded annually and he will be able to withdraw $4,000 per month for 30 years with the first withdrawal occurring on his 65th birthday. How much does Raj’s monthly deposit need to be in order to meet his retirement goals?

Let us first organize this information into a time diagram:

Next, we need to determine where to start. For back-to-back annuities, always start where the known payment is. In this example, we know the size of Raj's withdrawals during his retirement (PMT2), therefore, we will "start" with part 2.

Let us now fill in the BAII Plus table for Part 2:

| B/E | P/Y | C/Y | N2 | I/Y | PV2 | PMT2 | FV2 |

|---|---|---|---|---|---|---|---|

| BGN | 12 | 1 | 30×12=360 | 4 | CPT +847,893.56 | −4,000 | 0 |

- Because the withdrawals start right on Raj’s 65th birthday, BGN is on.

- Raj's makes monthly withdrawals but the interest compounds annually so P/Y = 12 and C/Y = 1. Be careful when entering a different value into P/Y than C/Y in your BAII Plus.

- Raj wants to withdraw $4,000 per month for 30 years so N2 = 30×12 and PMT2 = −4,000 (remember to make withdrawals negative).

- We assume there is nothing left in the account at the end of 30 years (FV2 = 0) because we are not told otherwise.

- The present value (PV2) becomes $847,893.56. This means that Raj will need $847,893.56 in his account when he retires in order to withdraw $4,000 per month for 30 years.

- The present value from the second annuity will become the future value for the first annuity but we change its sign

- Enter FV1 as negative. Ie: PV2 = −FV1. This is because FV1 is will be considered as the final withdrawal when ending annuity1.

We can now calculate the size of Raj's monthly deposits (PMT1). Let us fill in the BAII Plus table for Part 1:

| B/E | P/Y | C/Y | N1 | I/Y | PV1 | PMT1 | FV1 |

|---|---|---|---|---|---|---|---|

| BGN | 12 | 1 | 40×12=480 | 6 | +1,000 | CPT +436.95 | −847,893.56 |

- Because the deposits start today, BGN is on for part 1.

- Again, Raj makes monthly payments and the interest is compounded annually, so P/Y = 12 and C/Y = 1.

- Because Raj makes monthly deposits for 40 years, N1 = 40×12 = 480.

- Finally, be careful of the signs for PV and FV. They must be opposite in sign.

- We will make PV1 positive (as it is an initial deposit) and FV1 negative (we treat it as a withdrawal at the end).

Conclusion: Raj needs to deposit $436.95 per month for the next 40 years to achieve his retirement goals.

Interest Earned on Back-to-Back Annuities

Again we use the usual interest formula:

[latex]\begin{align*} \textrm{Interest Earned} &= \textrm{Money Out} - \textrm{Money In} = \textrm{\$ OUT} - \textrm{\$ IN} \end{align*}[/latex]

We need to be careful when calculating money in and money out for deferred annuities.

- All deposits are considered money in ($ IN).

- All withdrawals are both money out ($ OUT).

- Do not include FV1 nor PV2 in the $ IN or $ OUT calculations.

- Because FV1 does not get withdrawn but instead becomes the starting balance for the annuity (PV2), it is not considered money out.

- Similarly, because PV2 does not get deposited but instead is actually the ending balance from annuity1 (FV1), it is not considered money in.

| PV1 | Interest1 | PMT1 | FV1 | PV2 | Interest2 | PMT2 | FV2 |

|---|---|---|---|---|---|---|---|

| Initial Deposit | + % Earned | + Regular Deposits | =Ending Balance Part 1 | =Starting Balance Part 2 | + % Earned | = Regular Withdrawals | + Final Withdrawal |

| $ IN | $ IN | $ IN | –– | –– | $ IN | $ OUT | $ OUT |

This gives us the following equation for interest earned:

[latex]\begin{align*} \textrm{Interest Earned} &= \textrm{\$ OUT} - \textrm{\$ IN}\\ &=(\textrm{Regular Withdrawals}+\textrm{Final Withdrawal}) - (\textrm{Initial Deposit}+\textrm{Regular Deposits})\\ &= ( \textrm{PMT}_2\times\textrm{N}_2+\textrm{FV}_2)-(\textrm{PV}_1+\textrm{PMT}_1\times\textrm{N}_1) \end{align*}[/latex]

Example 5.6.2

How much interest will Raj earn over the 70 years that his money is invested in Example 1a?

The Money Out, in this case, is the amount that Raj withdraws during his retirement:

[latex]\begin{align*} \textrm{\$ OUT} &= \textrm{Regular Withdrawals}+\textrm{Final Withdrawal} \\ &= \textrm{PMT}_2\times\textrm{N}_2+\textrm{FV}_2 \\ &= \$4,000\times 360+0 \\ &= \$1,440,000 \end{align*}[/latex]

The Money In is the amount Raj deposits into the account:

[latex]\begin{align*} \textrm{\$ IN} &= \textrm{Initial Deposit}+\textrm{Regular Deposits} \\ &= \textrm{PV}_1+\textrm{PMT}_1\times\textrm{N}_1 \\ &= \$436.95\times 480+\$1,000 \\ &= \$210,736 \end{align*}[/latex]

Now take the difference between the money out and the money in (notice that neither FV1 nor PV2 are included in the $ OUT nor $ IN calculations):

[latex]\textrm{Interest Earned}= \$1,440,000 - \$210,736 = $1,229,264[/latex]

Conclusion: Raj will earn $1,229,264 in interest over the 70 years that his money is invested!

Switching from BGN to END

Let us examine Raj's retirement example (Example 1a) once again. In Example 1a, BGN was turned on for both annuity1 and annuity2. This was because Raj's first deposit was made immediately (at the start of annuity1) and his first withdrawal was made exactly on this 65th birthday (at the start of annuity2). Let us now look at an example where BGN is turned off (ie: the calculator is set to END).

Example 5.6.3

What would change if Raj withdrew his first retirement payment of $4,000 (PMT2) two months after his last deposit (last PMT1)? How much would Raj need to deposit into the retirement fund each month (PMT1) in this case?

Because Raj made his deposits into the saving account (annuity1) at the beginning of each month then the last deposit would go into the account one month before his 65th birthday. His first withdrawal occurs two months after this last deposit. That means the first withdrawal occurs one month after his 65th birthday, which would be the end of the first payment interval for annuity2. That means we set BGN to off (END) for annuity2. Let us look at the new timeline for this question:

Notice that turning BGN ‘off’ (setting the calculator to END) will change the value of PV2 for annuity2. Let us start by re-calculating the value of PV2:

| B/E | P/Y | C/Y | N2 | I/Y | PV2 | PMT2 | FV2 |

|---|---|---|---|---|---|---|---|

| END | 12 | 1 | 30×12=360 | 4 | CPT +845,126.83 | −4,000 | 0 |

Then, let’s use the value for PV2 in FV1 but make FV1 negative. Don't forget to turn BGN on for this calculation:

| B/E | P/Y | C/Y | N1 | I/Y | PV1 | PMT1 | FV1 |

|---|---|---|---|---|---|---|---|

| BGN | 12 | 1 | 40×12=480 | 6 | +1,000 | CPT +435.50 | −845,126.83 |

Conclusion: Raj will need to deposit $435.50 per month into his retirement fund.

Check Your Knowledge for Example 1c

Lump Sum Deposits

It is possible to either deposit or withdrawal money between annuities. Let us again examine Raj's retirement example and see what happens if Raj deposits additional money into his retirement savings account when he turns 65.

Example 5.6.4

Raj anticipates downsizing (selling his house and buying a smaller property) when he turns 65. He thinks he can deposit $100,000 from the sale of his property into his retirement savings plan when he turns 65. How much are Raj’s new monthly deposits into his savings plan (annuity 1) with this extra deposit into the retirement fund? Use the values from part c) and add the extra $100,000 deposit when Raj turns 65.

Let us first look at the timeline for this question:

Let us next examine the BAII Plus Table for Annuity2.

Annuity 2 (Regular Withdrawals):

| B/E | P/Y | C/Y | N2 | I/Y | PV2 | PMT2 | FV2 |

|---|---|---|---|---|---|---|---|

| END | 12 | 1 | 30×12=360 | 4 | CPT +845,126.83 | −4,000 | 0 |

Notice that nothing changes for Annuity2 between examples 1c and 1d (PV2 does not change). Where example 1d differs is in Annuity1.

All together, Raj needs $845,126.83 saved up at the start of annuity2 (PV2). He receives an extra $100,000 from the sale of his property at that time. This means he only needs to save $745,126.83 during Annuity1. This will be the value of FV1:

[latex]\begin{align*}\textrm{PV}_2 &= \$845,126.83 \\ &= \$745,126.83+\$100,000.00\\ &= \textrm{FV}_1+\$100,000.00 \end{align*}[/latex]

We can see, above, that FV1 must equal $745,126.83. Let us write out the formal equation to solve for FV1when there is a lump-sum deposit between annuities:

[latex]\textrm{FV}_{1} = \textrm{PV}_{2}-\textrm{Lump Sum Payment}[/latex]

Now that we know FV1, we can calculate the new value for PMT1.

Annuity 1 (Regular Deposits)

| B/E | P/Y | C/Y | N1 | I/Y | PV1 | PMT1 | FV1 |

|---|---|---|---|---|---|---|---|

| BGN | 12 | 1 | 40×12=480 | 6 | +1,000 | CPT +383.34 | −745,126.83 |

Conclusion: Raj will need to deposit $383.34 per month into his retirement fund.

Check Your Knowledge for Example 1d

Interest Earned with Lump Sum Deposits

When calculating interest earned on back-to-back annuity problems with lump-sum payments, there is an additional value we include in the money in ($ IN) — the lump sum deposit:

[latex]\begin{align*} \textrm{\$ IN} &= \textrm{Initial Deposit} + \textrm{Regular Deposits} + \textrm{Lump Sum Deposit} \\ &= \textrm{PV}_{1} +\textrm{PMT}_{1}× \textrm{N}_{1} + \textrm{Lump Sum Deposit} \end{align*}[/latex]

The money out ($ OUT) does not change. Taking the difference between the money out and money in gives the following equation for interest earned on back-to-back annuities with lump-sum deposits:

[latex]\textrm{Interest Earned} = \left(\textrm{PMT}_2×\textrm{N}_2 + \textrm{FV}_2\right) - \left(\textrm{PV}_1 +\textrm{PMT}_1× \textrm{N}_1 + \textrm{Lump Sum Deposit} \right)[/latex]

Let us now look at Raj's retirement example again to see an example of this calculation.

Example 5.6.5

How much interest will Raj earn in over the 70 years of his retirement investment in Example 1d?

The $ IN will now include the additional $100,000 deposit as well as the initial deposit (PV1) and the regular monthly deposits (PMT1) into the savings account (annuity1):

[latex]\textrm{\$ IN} = \$1,000 + 480 × \$383.34 + \$100,000 = \$285,003.20[/latex]

The $ OUT will not change:

[latex]\textrm{\$ OUT} = 360 × \$4,000 = \$1,440,000[/latex]

Taking the difference between $ OUT and $ IN gives:

[latex]\text{Interest} = \$1,440,000 – \$285,003.20 = \$1,154,996.80[/latex]

Conclusion: Raj will earn $1,154,996.80 in interest over the 70 years that his money is invested.

Check Your Knowledge for Example 1e

Registered Education Savings Plan (RESP)

It is common when saving for a child’s education to save up by making regular deposits into an RESP (registered education savings plan). There is a grant called the Canada Education Savings Grant (CESG) that adds 20% to these regular deposits (up to a maximum of $500 per year). Let us examine how this grant works for Sofia's RESP in the example below.

Example 5.6.6

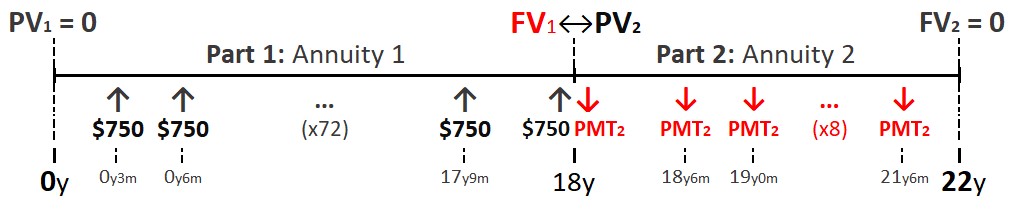

Dmitry and Elena just had a baby girl, Sofia. They set up an RESP for Sofia. Given below are the terms:

- They deposit $625 every quarter into the RESP

- The first deposit occurs 3 months after Sofia is born

- The last deposit occurs on Sofia's 18th birthday

- The deposits receive the CESG grant — 20% is added to each deposit by the government

- Sofia makes her first of 8 semi-annual withdrawals on her 18th birthday to attend university

- The education fund earns 4.25% compounded monthly for the entire time

What is the size of Sofia's semi-annual withdrawals?

Before we determine what to enter on the time diagram & BAII Plus, let’s ask a few important questions:

Key Questions to Get Started on Example 2

Let us gather all of this information into a timeline:

Always start where the known payment (PMT) is. We know that $750 per quarter will be deposited into the RESP (= PMT1). Therefore, "start" with Part 1.

Annuity 1 (Regular Deposits):

| B/E | P/Y | C/Y | N1 | I/Y | PV1 | PMT1 | FV1 |

|---|---|---|---|---|---|---|---|

| END | 4 | 12 | 18×4=72 | 4.25 | 0 | +750 | CPT −80,614.76 |

Enter the value for FV1 into PV2. Don't forget to make PV2 positive. We can now calculate PMT2:

Annuity 2 (Regular Withdrawals):

| B/E | P/Y | C/Y | N2 | I/Y | PV2 | PMT2 | FV2 |

|---|---|---|---|---|---|---|---|

| BGN | 2 | 12 | 4×2=8 | 4.25 | +80,614.76 | CPT −10,840.65 | 0 |

Conclusion: Sofia can withdraw $10,840.65 every 6 months to pay for university [1].

Lump Sum Withdrawals

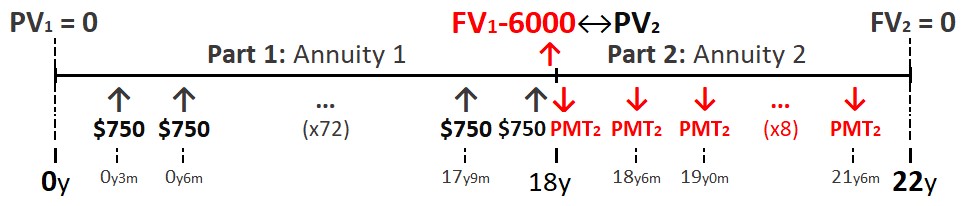

Let us now examine the scenario where a lump-sum withdrawal occurs between annuities. We will see what happens if Sofia makes a lump-sum withdrawal on her 18th birthday in the example below:

Example 5.6.7

Redo Example 2 but add the following: on Sofia's 18th birthday, she purchases a car for $6,000. Because she will be using the car to get to and from university, she is able to withdraw $6,000 from her RESP fund. What will be the size of her new semi-annual withdrawals if everything else remains the same on Sofia’s RESP account?

With the new $6,000 withdrawal when Sofia turns 18, the timeline will now become:

The value of FV1 will remain the same:

Annuity 1 (Regular Deposits):

| B/E | P/Y | C/Y | N1 | I/Y | PV1 | PMT1 | FV1 |

|---|---|---|---|---|---|---|---|

| END | 4 | 12 | 18×4=72 | 4.25 | 0 | +750 | CPT −80,614.76 |

Now, let's use the value of FV1 to calculate PV2.

[latex]\begin{align*}\textrm{PV}_2 &= \textrm{FV}_1 - \$6,000 \\ &= \$80,614.76-\$6,000\\ &= \$74,614.76 \end{align*}[/latex]

We can now enter $74,614.76 in for PV2 and calculate the new value for PMT2.

Annuity 2 (Regular Withdrawals):

| B/E | P/Y | C/Y | N2 | I/Y | PV2 | PMT2 | FV2 |

|---|---|---|---|---|---|---|---|

| BGN | 2 | 12 | 4×2=8 | 4.25 | +74,614.76 | CPT −10,033.80 | 0 |

Conclusion: Sofia can now withdraw $10,033.80 every 6 months from her RESP fund.

Interest Earned with Lump Sum Withdrawals

When calculating interest earned on back-to-back annuity problems with lump-sum withdrawals, there is an additional value we include in the money out ($ OUT) — the lump sum withdrawal:

[latex]\begin{align*} \textrm{\$ OUT} &= \textrm{Lump Sum Withdrawal + Regular Withdrawals + Final Withdrawal}\\ &= \textrm{Lump Sum Withdrawal}+\textrm{PMT}_{2}× \textrm{N}_2 +\textrm{FV}_{2} \end{align*}[/latex]

The money in ($ IN) does not change. Taking the difference between the money out and money in gives the following equation for interest earned:

[latex]\textrm{Interest Earned} = (\textrm{Lump Sum Withdrawal}+\textrm{PMT}_{2}× \textrm{N}_{2} + \textrm{FV}_{2}) - (\textrm{PV}_{1} +\textrm{PMT}_{1}× \textrm{N}_{1})[/latex]

Let us now look at Sofia's RESP example again to see an example of this calculation.

Example 5.6.8

How much interest does Sofia’s RESP account earn in Example 2b over the 22 years?

Let us first calculate the Money In to the RESP account over the 22 years:

[latex]\text{Money In} = 72 \times $750 = $54,000[/latex]

The Money Out will include the $6,000 withdrawal:

[latex]\text{Money Out} = \$6,000 + 8 \times $10,033.80 = $86,270.40[/latex]

Taking the difference between the Money Out and In gives:

[latex]\text{Interest} = $86,270.40 – $54,000 = $32,270.40[/latex]

Sofia’s RESP will earn $32,270.40 in interest over the 22 years that the money is invested.

Final Withdrawals

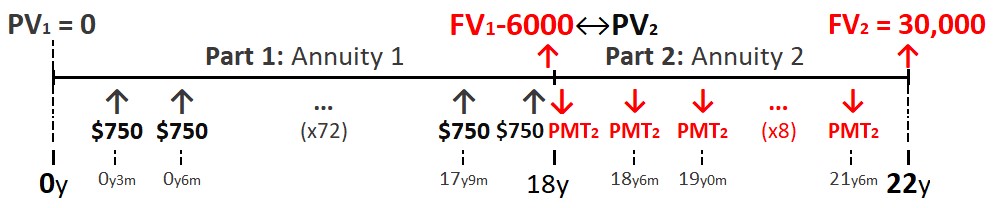

Let us finish this (very long) section with one final topic — money left over at the end. If there is any money over at the end of a back-to-back annuity, this amount will be entered into FV2 and we make it negative (it is treated as a final withdrawal). Let us look again at Sofia's RESP example and assume Sofia wants money left over at the end.

Example 5.6.9

Redo Example 2b but assume Sofia wants $30,000 left in her RESP after she graduates from university to help pay for her MBA. Calculate the size of her semi-annual withdrawals in this case.

With the $30,000 left at the end, the timeline now becomes:

All of Annuity1 will remain the same as well as PV2 (the same as in Example 2b). We will start our calculations with Annuity2. Almost all of the values are the same except FV2: enter the ending balance amount ($30,000) into FV2 and make it negative, Then calculate Sofia's new withdrawal size (PMT2):

Annuity 2 (Regular Withdrawals):

| B/E | P/Y | C/Y | N2 | I/Y | PV2 | PMT2 | FV2 |

|---|---|---|---|---|---|---|---|

| BGN | 2 | 12 | 4×2=8 | 4.25 | +74,614.76 | CPT −6,629.23 | −30,000 |

Conclusion: Sofia can withdraw $6,629.33 every 6 months and still have $30,000 left over at the end.

Your Own Notes

- Are there any notes you want to take from this section? Is there anything you'd like to copy and paste below?

- These notes are for you only (they will not be stored anywhere)

- Make sure to download them at the end to use as a reference

The Footnotes

- The current maximum allowable withdrawal amount on RESP's is $5,000 in the first quarter while attending post-secondary. Let's assume that this maximum allowable amount will increase in 18 years once Sofia attends university. ↵

Registered Retirement Savings Plan

Registered Education Savings Plan

The CESG provides 20% of the Registered Education Savings Plan (RESP) contributions of up to $2,500. That means the CESG can add a maximum of $500 to an RESP each year.