6.3 Net Present Value

Suppose that we set a minimum rate of return of 6% effective and apply it to our first example. Then, the future inflows would have present values of:

[latex]\frac{$13,000}{1.06}=$12,264.15[/latex]

And

[latex]\frac{$8,000}{1.06^2} =$7,119.97[/latex]

So $12,264.15 is the amount it is worth investing now to receive $13,000.00 in one year (and earn 6%), and $7,119.97 is the amount it is worth investing now to receive $8,000.00 in two years (and earn 6% compounded annually).

Thus, to earn a rate of return of 6% per year, it would be worth paying a total of:

[latex]$12,264.15 +$7,119.97 = $19,384.12[/latex]

But the investment costs $20,000, which is $615.88 more than it should if 6% is to be earned! Consequently, the investment should not be made if 6% is the minimum acceptable rate.

The discounting procedure above finds the Net Present Value (NPV) of investments. This dollar amount is the difference between what "should" be worth investing and what actually has to be invested. So the inflows (benefits) are discounted to see the maximum amount worth investing, and the outflows (costs) are discounted to see what actually is being invested.

Using PV for present value:

[latex]NPV = PV (inflows)-PV (outflows)[/latex]

Example 6.3.1

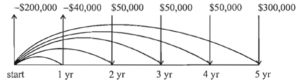

A small manufacturing business will cost $200,000 paid immediately and other expenses incurred are expected to result in a net negative cash flow of $40,000 by the end of the first year. It is then expected to earn annual positive net cash flows of $50,000 starting at the end of the second year and continuing each year until the end of the fifth year. It will be sold at the end of the last year (year five) for $250,000.

If the investors have set a minimum rate of return of 20%, should they invest in the business?

To evaluate this investment by NPV we find the outflows:

| PV of $200,000 | is | $200,000.00 |

| PV of $40,000 (yr 1) | is | $33,333.33 |

| Total PV Outflows | $233,333.33 | |

| PV of $50,000 (yr 2) | is | $34,722.22 |

| PV of $50,000 (yr 3) | is | $28,935.19 |

| PV of $50,000 (yr 4) | is | $24,112.65 |

| PV of $300,000 (yr 5) | is | $120,563.27 |

| Total PV Inflows | $208,333.33 |

So that:

[latex]\begin{align*} NPV &= PV (inflows)-PV (outflows)\\ &=$208,33.33-$233,333.33\\ &=-$25,000 \end{align*}[/latex]

The negative NPV shows that the investment did not earn the required rate of return.

Note that the net outflow of $40,000 in year 1 was also discounted to its present value of $33,333.33 to make the evaluation. You could assume that if $33,333.33 were invested elsewhere it would earn 20% and be available as $40,000 at year 1.

To summarize decisions based on NPV:

- If, for a given required rate of return, an investment has NPV > 0 (i.e., a positive net present value), then the investment earns more than the required rate.

- If NPV < 0 (i.e., a negative net present value), then the investment earns less than the required rate.

- If NPV = 0, then the investment earns exactly the required rate.

Be careful to note that a negative NPV does not necessarily imply that the investment resulted in a loss. It may be that the investment earned a profit, but did not do so fast enough to make the required rate of return. This was the case in the example above, which would have had a profit of $210,000, but would not have made the profit at a rate of 20% effective.

Knowledge Check 6.1

To check the result of the last example, complete the following "account" calculation at 20% effective.

| Time | Interest | Deposit | Withdrawal | Balance | |||||

| 0 | $200,000 | $200,000 | |||||||

| 1 | $40,000 | 40,000 | ? | ||||||

| 2 | ? | 50,000 | ? | ||||||

| 3 | ? | 50,000 | ? | ||||||

| 4 | ? | 50,000 | ? | ||||||

| 5 | ? | 300,000 | ? | ||||||

You should find a final balance of $62,208 which shows that to earn 20% an extra $62,208 would be required at the end of the fifth year. This again shows that the original investment did not earn 20%.

Question: How is the required $62,208 related to the NPV of -$25,000?

Knowledge Check 6.2

Now consider the problem of choosing between two different investments, which might both be acceptable when considered separately.Suppose the investors in Example 2, who are considering the manufacturing business, have also the choice of purchasing a share in an existing business, which is described below. If they have set a minimum rate of return of 15%, how can we determine which investment is preferable?

Example 6.3.2

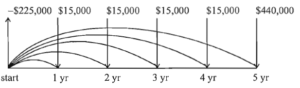

The share of the existing business would cost $225,000 cash and is expected to produce cash inflows of $15,000 a year for five years, then to be sold for $425,000.

For the share investment we have the following cash diagram:

To evaluate this investment by NPV at 15% effective, we have for the only outflow a present value of $225,000, and for the inflows:

| Time (year) | Inflow | PV |

| 1 | $15,000 | $13,043.48 |

| 2 | 15,000 | 11,342.15 |

| 3 | 15,000 | 9,862.74 |

| 4 | 15,000 | 8,576.30 |

| 5 | 440,000 | 218,757.76 |

| Total PV Inflows | $261,582.43 |

Then the net present value is:

[latex]\begin{align*} NPV &=$261,582.43-$225,000\\ &=$36,582.43 \end{align*}[/latex]

In Knowledge Check 6.2 you should have found that at 15% the NPV of the manufacturing investment is $13,641.07; hence, by this criterion the purchase of the share would be more profitable.

Knowledge Check 6.3

Use the net present value criterion to evaluate the following investments:

OPTION A: A small restaurant business in leased premises can be purchased for $30,000. It is expected to produce cash inflows from operations of $12,000 a year (at the end of each year) for 4 years. At the end of the 4 years the lease will expire and the equipment will be sold for $14,000.

OPTION B: A similar restaurant with its own premises can be purchased for $92,000. It would produce net cash inflows of $21,000 at the end of each year for 5 years and would be sold for $95,000 at that time.

If the prospective investors set a minimum rate of return of 20%, should they purchase a restaurant, and if so, which one would be the best deal?

You should attempt the problem by discounting each cash flow and finding the NPV that way. In the following setup for OPTION A, we have assumed that outflows will be treated as negative. This is a standard practice and allows a straightforward total to get NPV.

| Time (yr) | Cash Flow | PV |

| 0 | -$30,000 | ? |

| 1 | 12,000 | ? |

| 2 | 12,000 | ? |

| 3 | 12,000 | ? |

| 4 | 26,000 | ? |

| (12,000 + 14,000) | ||

| NPV = | $7,816.36 |

For OPTION B you should get an NPV of $8,981.22.

On the basis of NPV both restaurants are acceptable investments, but the second restaurant (OPTION B) would be the most beneficial if only one is to be purchased.

Calculating the present value of the inflows can always be done by discounting each flow separately, but in the case of equal flows it can also be done by an annuity. For example, in OPTION A the first three cash flows of $12,000 can be treated as an annuity by setting:

[latex]n = 3;\;i = 20%;\;PMT = $12,000;\;FV = 0[/latex]

and finding PV. Then find the present value of the final $26,000 at year 4. You should get a total of $37,813.36, which agrees with the result above.

Your Own Notes

- Are there any notes you want to take from this section? Is there anything you'd like to copy and paste below?

- These notes are for you only (they will not be stored anywhere)

- Make sure to download them at the end to use as a reference

The sum of all Inflows, minus all Outflows, adjusted for time.